Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL) has been gently sleeping, underestimated by the roaring crowds of Wall Street. As the year ticks by, its revenue growth leaps, margins tighten, yet the stock sits unnoticed, unloved in comparison to its flashier tech brethren.

Currently holding the unassuming fifth spot, Alphabet has watched Nvidia and Amazon breeze past it with uncanny regularity. But as the tide turns, Alphabet stands on the cusp of a unique blend – value and growth, potentially poised to offer investors a ride to the stars.

But can it truly be the millionaire maker?

Alphabet’s Symphony of Success

Alphabet reigns as the parent of digital royalty – Google, YouTube, and Android. Their shared melody? Advertising. Making up a resounding 76% of revenue, this segment weathered the 2022-2023 storm of economic tremors with grace and now gleams with newfound strength.

In the fourth quarter, Alphabet’s ad revenue soared by 11%, guided by YouTube’s stellar 16% growth. YouTube, not to be outdone, boasts the crown jewel of an ad business, claiming a whopping 9% of U.S. streaming time – surpassing Netflix and even Disney+. This powerful platform promises sustained growth as advertisers flock to its fruitful shores.

A further crescendo awaits in the realm of cloud computing. While Google Cloud stands third behind Amazon Web Services and Microsoft Azure, it commands 11% of the market share, a slice set to grow from $626 billion in 2023 to a hefty $1.3 trillion by 2028.

And let’s not forget the secret sauce – artificial intelligence (AI). Alphabet’s own gem, Gemini, a generative AI model, shines bright. Topping the charts, outperforming competitors like OpenAI’s ChatGPT, Gemini’s potential for revenue boost across Alphabet’s ventures and internal bliss is immense.

Alphabet dances the steps of success elegantly. Yet, in the shadow of admiration, how overlooked is its stock?

Alphabet’s Stealthy Stock Valuation

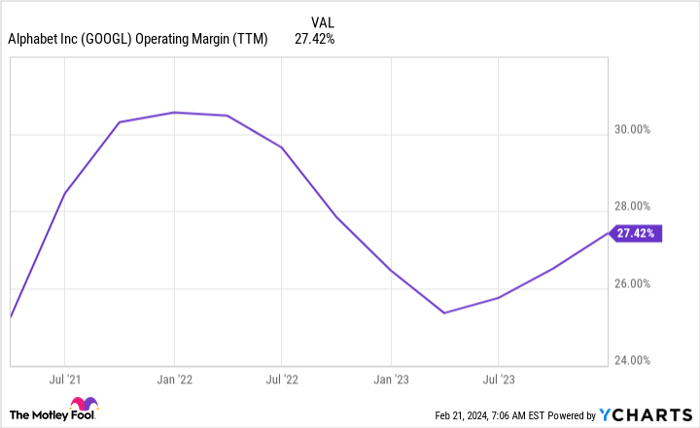

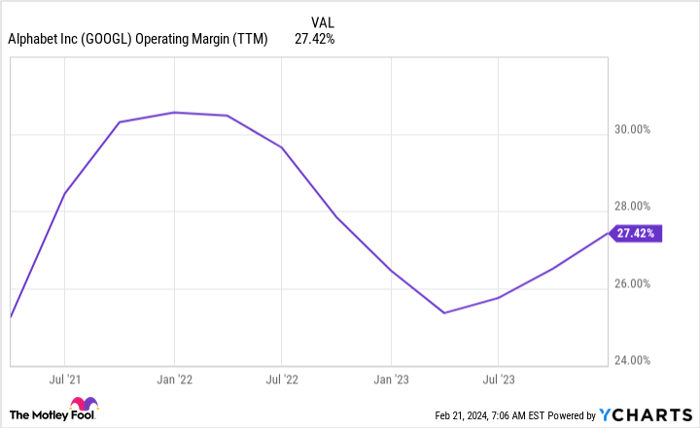

Despite strides in boosting margins via strategic layoffs and efficiency drives, Alphabet’s stock journey is far from over. Whispers of new layoffs swirl, marking a point in Google’s evolution where AI reigns supreme, poised to enhance margins to the levels seen at the peak of 2022.

GOOGL Operating Margin (TTM) data by YCharts. TTM = trailing 12 months.

If profits outpace revenue growth, each quarter will unveil Alphabet’s stock as a hidden gem. Priced at a humble 21 times forward earnings, it now stands a bargain compared to previous years.

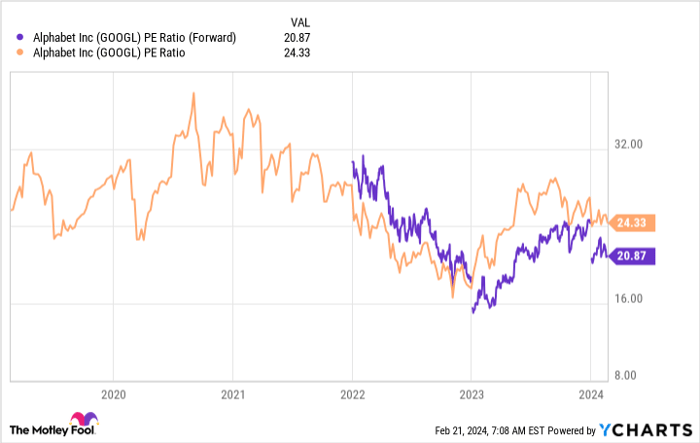

GOOGL PE Ratio (Forward) data by YCharts. PE = price to earnings.

With the S&P 500 sporting a forward price-to-earnings (P/E) ratio around 20.4, Alphabet’s stock snuggles close to the cozy norm. Grooving at a 13% revenue growth clip, tightening margins, and leading in AI, Alphabet oozes more than just average appeal.

It’s only fair to whisper that Alphabet’s stock is quietly undervalued. If awarded the same premium as Microsoft at 34 times forward earnings, Alphabet would don a $2.9 trillion market cap – a regal perch as the second-largest company globally.

For now, Alphabet remains touted by a select few, a hidden gem ripe for the plucking. But can it pave your road to riches? The dream, though faint, whispers that Alphabet’s stock’s muted roar, mixed with its growth potential, could indeed amplify your portfolio on the path to the promised land of wealth.

Should you invest $1,000 in Alphabet right now?

Before you tango with Alphabet’s stock, heed this: The Motley Fool Stock Advisor analysts have uncovered what they believe are the 10 best stocks for now, with Alphabet notably absent. These chosen few promise to make the ground tremble with potential returns in the years ahead.

Stock Advisor offers a map to the treasure – a blueprint for success, filled with portfolio wisdom, analyst insights, and twin stock picks every month. Since 2002, this service has tripled the S&P 500’s returns*.

Explore the 10 stocks

*Stock Advisor returns as of February 20, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet and Microsoft. It also recommends options like long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool follows a strict disclosure policy.

The views and opinions expressed herein belong to the author and may not reflect those of Nasdaq, Inc.