Uber’s Q3 Performance: Highlights and Challenges Ahead

On Oct. 31, Uber Technologies (UBER) announced its third-quarter 2024 results, surpassing earnings expectations and revenues prior to the market opening. This marked the second consecutive quarter of outperforming forecasts after a disappointing loss in the first quarter of 2024. Notably, UBER achieved over $1 billion in operating income (on a GAAP basis) for the first time during the September quarter, amplifying investor optimism.

With these positive results, investors may wonder if now is the right time to purchase UBER stock. To answer this, let’s first analyze UBER’s latest quarterly performance.

Overview of UBER’s Q3 Results

In Q3, UBER reported earnings per share of $1.20, significantly outperforming the Zacks Consensus Estimate of 41 cents and more than doubling year-over-year. Total revenue reached $11.2 billion, exceeding expectations of $10.9 billion. This represented a 20% increase year-over-year, or 22% on a constant currency basis.

Check out the latest EPS estimates and surprises on ZacksEarnings Calendar.

As economic activities return to pre-pandemic levels, commuting and travel demand have rebounded. This resurgence has resulted in robust performance for UBER’s Mobility business, with segment revenues soaring 26% in the September quarter.

The uptick in customer traffic contributed to an impressive gross bookings figure, which jumped 17% year-over-year in the Mobility segment, totaling $21 billion during the quarter.

Additionally, UBER’s Delivery sector saw segment revenues rise 18% compared to last year, with gross bookings climbing 16% annually to $18.7 billion.

Overall, trips surged 17%, equating to approximately 2.9 billion trips, averaging about 31 million rides daily.

Concerns About Slow Bookings Growth

Despite these encouraging results, UBER shares fell 7.5% following the earnings announcement on Oct. 31. Investors expressed disappointment over a slower-than-expected growth projection. The forecast for Q4 2024 predicts gross bookings between $42.75 billion and $44.25 billion, reflecting a constant currency growth rate of 16-20% from Q4 2023.

The anticipated year-over-year growth in trips for the last quarter is expected to mirror the 3Q results. This outlook, which factors in approximately a two percentage point currency headwind, was seen as conservative and contributed to the drop in share price.

In the latest quarter, total gross bookings rose 16% year-over-year to $41 billion. This growth rate was lower than the 19% growth seen in the previous quarter, raising concerns about a potential slowdown. The Mobility segment, a primary driver of UBER’s business, delivered gross bookings of $21 billion in Q3, falling short of the $21.7 billion target. Furthermore, growth in the Mobility unit slowed from 23% in Q2 to 17% in Q3.

These figures highlight potential slowdowns which could influence UBER’s strategy moving forward. Given its dominance in North American ride-sharing, UBER might focus more on suburban expansion to combat market saturation fears.

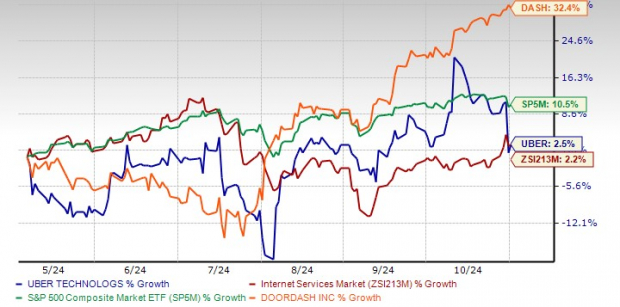

The lack of announcements about share repurchases also disappointed investors, adding to the post-earnings decline. Over the past six months, UBER shares underperformed not only the S&P 500 index but also relative to its competitor DoorDash (DASH).

Comparing Six-Month Stock Prices

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Investor Guidance Following Q3 Earnings

To mitigate risks, diversification is key for large companies, and UBER has excelled in this area through strategic acquisitions and innovation. While the primary focus of UBER remains ride-sharing, it has branched out into food delivery and freight services.

The company’s expansion into international markets is beneficial for geographical diversification. Their commitment to prudent investments enhances service offerings and operational efficiency. However, concerns about the slowdown in gross bookings overshadow these positive developments.

Currently, UBER’s overall valuation seems high, reflected in a Value Score of D, indicating potential risk. The stock trades at a forward 12-month Price/Earnings ratio of 34.44X, compared to the industry’s 20.48X.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Compared to Lyft (LYFT), which trades at 14.02X, UBER shares appear more expensive. Moreover, UBER’s long-term debt rose by 31.5% to $11 billion as of Q3 2024, compared to figures from 2019, adding to the concerns about financial stability.

Analysis of Long-Term Debt to Capitalization

Image Source: Zacks Investment Research

Currently, UBER holds a Zacks Rank #3 (Hold), suggesting investors may find it prudent to wait for a more favorable entry point before purchasing shares following these earnings results.

Expert Stock Picks for Future Growth

Five Zacks analysts have selected their top picks that they believe could double in value within the coming months. Among these, Director of Research Sheraz Mian highlights one stock with tremendous potential for growth, particularly appealing to millennial and Gen Z consumers and generating nearly $1 billion in last quarter’s revenue.

With a recent dip in stock price, now might be an opportune time to invest. While not every recommendation guarantees success, this pick has the potential to exceed past Zacks favorites like Nano-X Imaging, which surged +129.6% in just over nine months.

Free: Discover Our Top Stock and More

Interested in the latest recommendations from Zacks Investment Research? Download 5 Stocks Set to Double for free.

Lyft, Inc. (LYFT): Free Stock Analysis Report

Uber Technologies, Inc. (UBER): Free Stock Analysis Report

DoorDash, Inc. (DASH): Free Stock Analysis Report

To read this article on Zacks.com, click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.