The cybersecurity darling, SentinelOne (NYSE: S), has been on fire throughout 2024. The stock soared, more than doubling from its 52-week low of $12.43 last June to a heart-fluttering high of $30.76 this past Valentine’s Day, fueled by Bank of America‘s decision to upgrade the stock from neutral to buy. As the shares continue to flirt near this peak, the burning question that lingers is whether the time is ripe to invest in SentinelOne.

Replicating Sherlock Holmes, let’s delve deeper into this digital mystery before making any financial commitments. The date to be marked on the calendar is March 13 when SentinelOne unveils its fiscal fourth-quarter results, painting a clearer picture of the company’s financial landscape.

Standing Tall in the Cybersecurity Arena

SentinelOne dances in the cybersecurity sector, a battleground where shields against cyber threats are indispensable. From safeguarding websites to shielding customer data, the cybersecurity industry is estimated to crack the $183 billion mark in 2024, escalating to a hefty $274 billion by 2028. This relentless demand spells good fortune for SentinelOne, providing a steady revenue stream for the company.

Yet, every silver lining harbors a cloud. Amidst the cybersecurity frenzy lies cutthroat competition, with players like CrowdStrike and Palo Alto Networks jostling for market share. Not to forget the tech giants – Microsoft, IBM, and Cisco Systems – who offer cybersecurity as part of their digital repertoire. The challenge, therefore, lies in SentinelOne’s ability to secure its ground amidst fierce competition.

So, how is SentinelOne faring in this digital duel, you ask? The company has shown prowess by multiplying its customer count. From a modest 4,700 customers pre-IPO in 2021 to a whopping 11,500 clients in the fiscal third quarter ending Oct. 31, 2023, SentinelOne’s customer growth chart has skyrocketed by 145% in just two-and-a-half years.

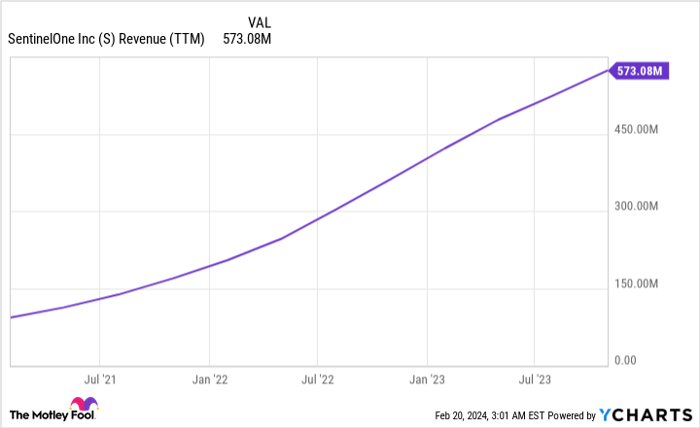

Charting Success with SentinelOne

Beyond customer stats, eyeing the company’s Annual Recurring Revenue (ARR) is akin to gazing into a crystal ball, signaling SentinelOne’s ability to not just attract new customers but also to nurture existing ones. With ARR hitting $663.9 million in fiscal Q3, a robust 43% leap year-over-year, this growth manifested in Q3 sales of $164.2 million, mirroring a 42% surge.

**Illustrative Chart Here**

Data by YCharts.

This revenue upswing is on a song and dance of its own. With fiscal Q4 revenue anticipated to scale $169 million, marking a double-digit jump from the $126.1 million the year before, SentinelOne remains on an upward trajectory, painting a picture of a company successfully luring clients with its cybersecurity expertise.

The company’s inception in 2013 wove artificial intelligence into its fabric. With an AI-driven defense mechanism – swiftly identifying and countering cyberattacks without human intervention – SentinelOne’s solution is not just quick, but a force to reckon with in the cybersecurity realm.

These AI capabilities have helped SentinelOne keep pace with the armory of cybercriminals, given AI’s ascendancy, much like ChatGPT’s emergence last year. In a twist of irony, SentinelOne recently unveiled a cyberattack software, harnessing ChatGPT to execute hacks using AI.

Down the Rabbit Hole with SentinelOne Stock

For all the cheers on customer and revenue growth, remember, SentinelOne is yet to turn a profit. Exiting fiscal Q3 with a net loss of $70.3 million, however, marks an optimistic shift from the previous year’s $98.9 million in the red. As the company steers towards profitability next year, cost-cutting measures are being meticulously etched into its blueprint.

Despite the formidable numbers, SentinelOne’s balance sheet tells a different tale. The balance sheet for fiscal Q3 gleamed like a polished diamond – with total assets amounting to a staggering $2.2 billion, towering over liabilities pegged at $615 million. The cherry on top? A treasury blooming with $1.1 billion in cash, cash equivalents, and investments.

Although SentinelOne’s stock has skyrocketed over the past year, it continues to flutter below its IPO price of $35. With robust fiscal Q4 results potentially nudging the stock to giddier highs than its recent 52-week peak, a twinkle in Bank of America’s eye glued a price target of $35 on the stock.

Considering SentinelOne’s rich tapestry of customer and revenue growth, its bottom line on the mend, and an enviable balance sheet, SentinelOne stock seems to wink like a sassy courtesan, beckoning investors to take the plunge.

Still on the fence about investing $1,000 in SentinelOne?

Before you take that leap, ponder over this anecdote:

The Motley Fool Stock Advisor team recently unveiled the holy grail – the 10 best stocks primed for primetime, with SentinelOne notably missing the cut. These golden stocks are believed to catapult returns to new heights in the coming years.

Stock Advisor isn’t just a roadmap but a treasure map, guiding investors to the pot of gold with monthly stock picks, analyst insights, and a track record that usually leaves the S&P 500 trail in the dust.*

Dive into the 10 stocks now!

*Stock Advisor returns as of February 20, 2024

Bank of America flirts with advertising through The Ascent, a Motley Fool subsidiary. Robert Izquierdo joins the Bank of America fan club alongside Cisco Systems, CrowdStrike, International Business Machines, Microsoft, and SentinelOne. While The Motley Fool swoons over Bank of America, Cisco Systems, CrowdStrike, Microsoft, and Palo Alto Networks, it woos investors with options, disclosing its intentions on Microsoft. And yes, there’s always a tale behind a feather. The Motley Fool prefers transparency and showcases its disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.