Energy Transfer LP: Analyzing Undervalued Stock Potential

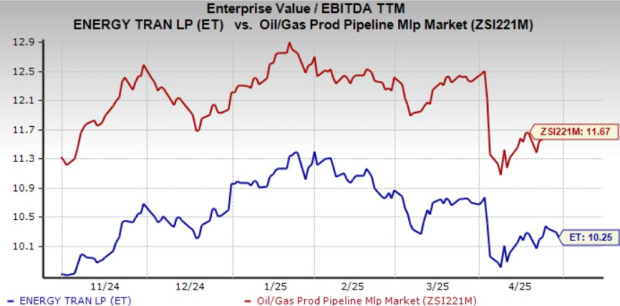

Energy Transfer LP (ET) units seem undervalued compared to the Zacks Oil and Gas Production Pipeline – MLB industry. Its current trailing 12-month Enterprise Value to EBITDA (EV/EBITDA) ratio is 10.25X, below the industry average of 11.67X. This indicates that ET is trading at a discount relative to competitors.

Energy Transfer operates an extensive pipeline network across the United States and is actively pursuing growth opportunities to meet increasing power demands.

Similarly, Plains All American Pipeline (PAA) is trading at a lower EV/EBITDA of 9.2X, also indicating a discount compared to its industry peers.

Image Source: Zacks Investment Research

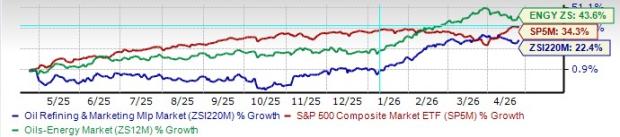

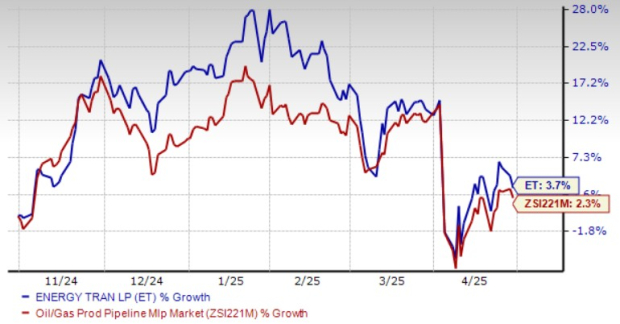

Over the past six months, ET stock has underperformed its industry.

Price Performance (Six Months)

Image Source: Zacks Investment Research

Should investors consider adding ET to their portfolios based solely on its discounted valuation and current price softness? An analysis of the underlying factors will aid in making an informed decision on investment viability.

Key Factors Impacting ET Stock Performance

Energy Transfer operates over 130,000 miles of pipelines across 44 states. The company is continuously expanding through both organic growth and strategic acquisitions. Since 2021, ET has completed a significant acquisition each year, including the purchase of WTG last year, enhancing its natural gas pipeline infrastructure in the Permian Basin.

Approximately 90% of Energy Transfer’s revenues come from fee-based contracts tied to transportation and storage services. These long-term agreements with a solid customer base provide stable cash flows and reduce exposure to commodity price fluctuations. As U.S. oil and gas production continues to rise, ET stands to benefit from increasing demand for pipeline services.

Additionally, Energy Transfer has significant export capabilities, with natural gas liquids (NGL) and crude oil export capacities exceeding 1.1 million and 1.9 million barrels per day, respectively. Ongoing expansion projects at its Marcus Hook and Nederland terminals are poised to further enhance this infrastructure. ET holds an estimated 20% share of the global NGL export market, indicating its strong position in international energy trade.

Strategically located across major U.S. production basins, Energy Transfer’s diverse asset base includes oil and gas pipelines, gathering and processing facilities, and storage assets. This diversification enables the company to efficiently serve various markets.

Cash Distribution to Unitholders

Energy Transfer currently offers a quarterly cash distribution rate of 32.75 cents per common unit. The company has increased its distribution rate 14 times in the last five years, although the current payout ratio is 101%.

Management Ownership Increases

Management and insiders hold a significant portion of ET units, with continued purchases by management and independent board members. Insiders acquired over 44 million units valued at $468 million between January 2021 and February 2025. This increasing insider ownership suggests positive growth prospects in the midstream sector.

Insider ownership in ET stock is nearly 10%, surpassing that of peers in the industry. This trend reflects confidence in the company’s future amidst rising midstream demand.

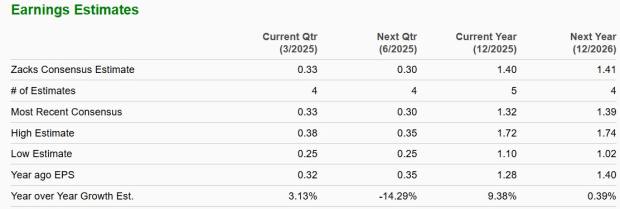

ET’s Earnings Estimates Project Growth

The Zacks Consensus Estimate for Energy Transfer’s earnings per unit indicates year-over-year growth of 9.38% and 0.39% for 2025 and 2026, respectively.

Image Source: Zacks Investment Research

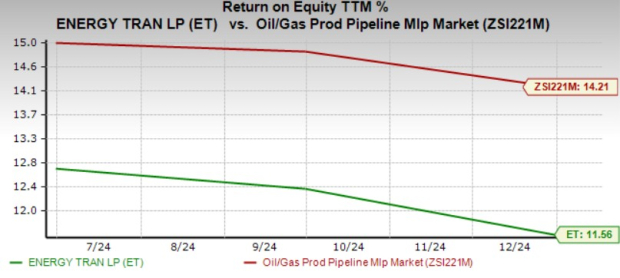

Low Return on Equity Compared to Industry

Energy Transfer’s trailing 12-month return on equity (ROE) stands at 11.56%, which is lower than the industry average of 14.21%. ROE measures how effectively a company uses shareholders’ funds to generate income.

Image Source: Zacks Investment Research

Conclusion

With a vast network exceeding 130,000 miles of pipelines across 44 states, Energy Transfer is well-positioned to leverage the increasing production of oil and natural gas within the U.S.

Despite its lower ROE compared to industry averages, current investors may opt to stay invested and benefit from the consistent cash distribution. Prospective investors may want to monitor the stock for a more favorable entry point.