MercadoLibre (MELI) is facing significant challenges to its profitability as it aggressively expands its first-party (1P) commerce operations. In Q1 2026, MELI’s 1P gross merchandise volume increased by 69% year-over-year on a foreign exchange neutral basis, largely driven by consumer electronics in Brazil. However, the rapid growth in inventory-led operations is causing a 300 basis point contraction in gross margin, leading to a 20% decline in operating income, which fell to $611 million.

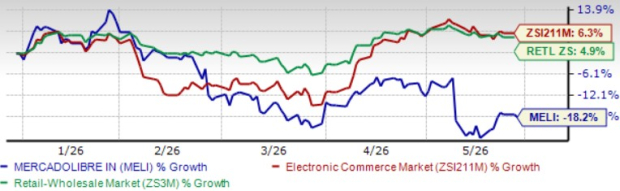

Despite the growth, the shift towards inventory-led commerce introduces a different cost structure, requiring substantial investments in fulfillment, logistics, and inventory management. MELI’s operating margin is now at 6.9%, and the company is prioritizing long-term scale over immediate profitability, suggesting that margin pressure may persist. Additionally, MELI’s shares have decreased by 18.2% year-to-date, while the broader Zacks Internet–Commerce and Retail-Wholesale sectors have seen positive returns of 6.3% and 4.9%, respectively.

The Zacks Consensus Estimate for MELI’s 2026 earnings is $40.97 per share, a decrease of 18.14% in the last 30 days but still indicative of a 3.98% annual increase. Currently, MELI has a Zacks Rank of #5 (Strong Sell).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.