Snowflake Shares Decline 18.1%, Struggling Against Industry Rivals

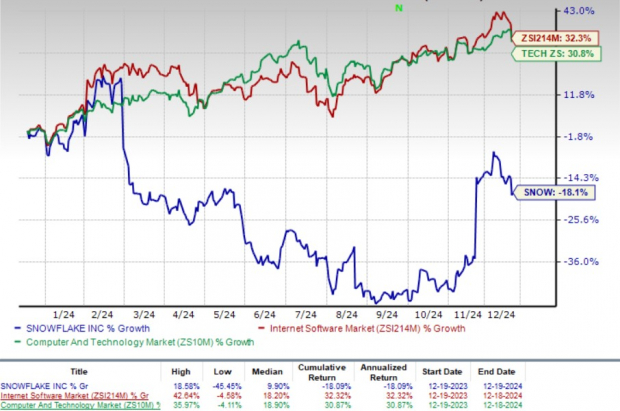

Snowflake SNOW shares have dropped 18.1% in the last year, significantly trailing the Zacks Computer & Technology sector, which has risen 30.8%, and the Zacks Internet – Software industry’s 32.3% return. This underperformance highlights the challenges facing the company.

Annual Stock Performance Review

Image Source: Zacks Investment Research

Currently, SNOW is considered overvalued, with a Value Score of F. It trades at a forward 12-month price/sales ratio of 12.5X, significantly higher than the industry average of 2.96X.

Forward Price/Sales Ratio Analysis

Image Source: Zacks Investment Research

Despite these challenges, Snowflake’s future looks bright, bolstered by a strong portfolio and a growing network of partners.

The stock is trading above both the 50-day and 200-day moving averages, which indicates a bullish market sentiment.

Bullish Trading Signals for SNOW

Image Source: Zacks Investment Research

Broad Capabilities Support SNOW’s Future

Snowflake’s position is strengthened by its wide-ranging capabilities, including Unistore, Marketplace Listing Auto-Fulfillment, Query Acceleration Service, geospatial analytics, Snowpark, and Snowpipe Streaming.

Innovations such as Iceberg, Hybrid tables, and the Cortex Large Language Model enhance SNOW’s offerings. In the third quarter of fiscal 2025, more than 3,200 accounts utilized SNOW’s AI and ML features, with approximately 500 adopting Iceberg.

Partnerships with companies like Amazon, Microsoft MSFT, ServiceNow NOW, NVIDIA, Fiserv, EY, Deloitte, LTMindtree, Next Pathway, and S&P Global broaden Snowflake’s ecosystem.

Recent collaborations with Microsoft and ServiceNow aim to enhance data interoperability, allowing customers to move data seamlessly and streamline application development.

Additionally, a partnership with Anthropic will integrate advanced AI models into Cortex AI to support secure and innovative AI applications. These strategies are designed to tackle significant market competition and alleviate pricing pressures in the evolving data landscape.

Prominent industry players like Disney DIS, Hyatt Hotels, Comcast, Accor, and Toyota depend on Snowflake’s platform, utilizing it for various operational enhancements.

The planned acquisition of Datavolo will further bolster Snowflake’s platform, enhancing its capabilities for structured and unstructured data while simplifying data engineering functions.

Positive Outlook from Earnings Estimates

For the fourth quarter of fiscal 2025, Snowflake anticipates product revenues between $906 million and $911 million, suggesting a 23% year-over-year increase.

The Zacks Consensus Estimate for these revenues is $952.55 million, equating to a 22.6% year-over-year rise.

Earnings estimates are set at 17 cents per share, representing a 41.67% increase over the last month but a 51.43% drop from the previous year.

In FY 2025, Snowflake forecasts a 29% revenue increase, aiming for $3.43 billion. Expectations for non-GAAP product gross margin are 76%, with a non-GAAP operating margin anticipated at 5%.

The Zacks Consensus Estimate for fiscal 2025 revenue is $3.59 billion, reflecting a 28% growth year-over-year.

The consensus mark for earnings stands at 68 cents per share, which is a 17.24% increase over the past month, though indicating a year-over-year decrease of 30.61%.

SNOW has exceeded earnings estimates in three of the last four quarters, with an average surprise of 35.39% on earnings.

Snowflake Inc. Price and Consensus

Snowflake Inc. price-consensus-chart | Snowflake Inc. Quote

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

Should You Buy, Sell, or Hold SNOW Stock?

Snowflake’s strengths lie in its solid portfolio, extensive partnerships, and growing client base; however, challenges from competitors, rising costs, and a stretched valuation are concerning.

Currently, SNOW holds a Zacks Rank #3 (Hold), suggesting that potential investors may want to wait for a more favorable entry point.

Zacks Predicts Top 10 Stocks for 2025

Interested in early tips on the best stocks for 2025?

History indicates their performance could be exceptional.

Since 2012, when Sheraz Mian took charge of the portfolio through November 2024, the Zacks Top 10 Stocks achieved an impressive gain of +2,112.6%, vastly outpacing the S&P 500’s +475.6%. Sheraz is currently evaluating 4,400 companies to select the top 10 stocks to hold in 2025. Make sure to seize this opportunity when the list is released on January 2.

Want the latest recommendations from Zacks Investment Research? Download 5 Stocks Set to Double for free.

Microsoft Corporation (MSFT): Free Stock Analysis Report

The Walt Disney Company (DIS): Free Stock Analysis Report

ServiceNow, Inc. (NOW): Free Stock Analysis Report

Snowflake Inc. (SNOW): Free Stock Analysis Report

For the full article on Zacks.com, click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.