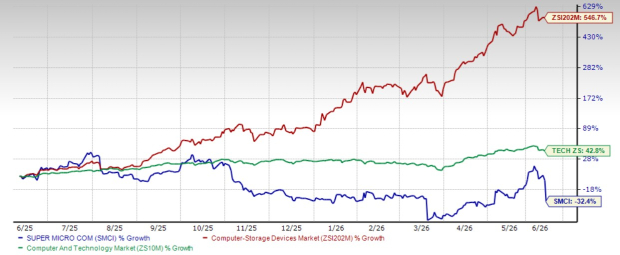

Super Micro Computer (SMCI) has seen its shares decline by 32.4% in the past year, significantly trailing the Zacks Computer-Storage Devices industry, which has risen by 546.7%, and the broader Computer and Technology sector, up 42.8%. Currently, SMCI is trading at a price-to-sales (P/S) ratio of 0.35x, compared to the industry average of 4.07x.

Despite its declining stock performance, SMCI benefits from soaring global AI infrastructure spending, with a backlog and record order activity driven by major customers such as NVIDIA and AMD. The company plans to scale its rack production capacity to over 6,000 AI racks monthly by fiscal 2026, as its global AI infrastructure facilities now support approximately 75 megawatts of capacity. However, SMCI faces challenges, including a striking increase in inventory to $11.1 billion and a reported negative operating cash flow of $6.6 billion during Q3 of fiscal 2026.

With over 80% of its revenues tied to AI GPU-related platforms and significant reliance on a few large clients, SMCI’s future remains uncertain amidst rising competition from major players like Dell Technologies and Hewlett Packard Enterprise. The Zacks Consensus Estimate for SMCI’s fiscal 2026 earnings per share stands at $2.56, marking a 24% year-over-year increase. Analysts currently recommend a “Hold” on SMCI stock until more favorable cash flow trends emerge.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.