Netflix Prepares for Q1 2025 Earnings Report Amidst Market Challenges

Netflix (NFLX) is set to announce its first-quarter 2025 earnings on Thursday.

Revenue and Earnings Projections

Netflix expects revenues to increase by 11% for the first quarter, which translates to a 14% growth on a constant currency basis. This projection falls slightly short of the company’s full-year guidance, largely due to price change timing and seasonal fluctuations in advertising revenue.

The streaming service aims for total revenues of $10.416 billion, reflecting an 11.2% year-over-year growth. In contrast, the consensus for revenues stands at $10.54 billion, suggesting a 12.5% year-over-year increase.

Regarding earnings, Netflix has forecasted profits of $5.58 per share. However, the Zacks Consensus Estimate is slightly higher at $5.74 per share, remaining unchanged over the past month.

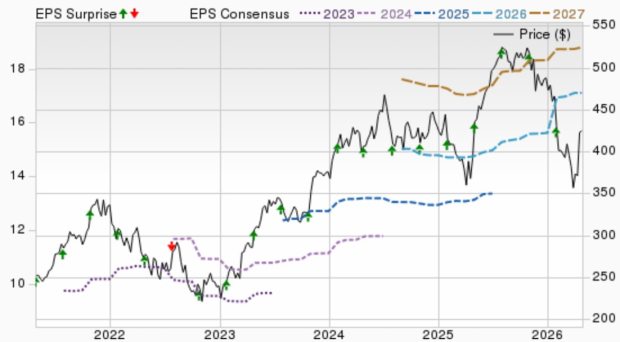

Image Source: Zacks Investment Research

Discover the latest earnings estimates and surprises on Zacks Earnings Calendar.

Earnings Surprise History

In the previous quarter, Netflix showcased an earnings surprise of 1.67%. The company has consistently outperformed the Zacks Consensus Estimate across the last four quarters, averaging a surprise of 7.17%.

Stock Price Performance

Netflix, Inc. price-eps-surprise | Netflix, Inc. Quote

Earnings Outlook for Netflix

Current indications suggest that Netflix may not exceed earnings expectations this quarter. A combination of a positive Earnings ESP and a Zacks Rank of #1 (Strong Buy), #2 (Buy), or #3 (Hold) usually increases the chances of an earnings surprise. Netflix is currently positioned with an Earnings ESP of -2.23% and a Zacks Rank #3.

Drivers Behind Upcoming Results

As Netflix approaches its Q1 2025 announcement, it might be wise for investors to hold their current positions. Although the company has shown robust growth—including gaining 19 million paid subscribers in the fourth quarter of 2024—first-quarter growth is typically slower due to seasonal effects and currency influences.

For the first quarter, the company is targeting an operating margin of 28.2%. The delay in growth can be attributed to the timing of price changes alongside a stronger U.S. dollar. Looking forward, Netflix maintains its content strategy, with popular series such as Squid Game and Stranger Things returning, and various new releases scheduled throughout 2025.

In addition, live content continues to grow in focus with WWE programming and plans for future NFL broadcasts. Furthermore, the ad-supported tier is gaining popularity, accounting for over 55% of sign-ups in available markets, promising additional monetization in the coming year.

The company is also expanding internationally with region-specific productions, which may boost global engagement amidst increased competition from players like Apple (AAPL), Amazon (AMZN), and Disney (DIS). Investors should weigh the potential impact of price increases on subscriber retention against these competition pressures before making any new investments.

Estimates for Q1 Growth

The Zacks Consensus Estimate predicts Netflix will add approximately 4.36 million paid streaming members in the first quarter of 2025. Specific revenue expectations across regions include:

- Asia-Pacific: Estimated revenue of $1.22 billion, showing a growth of 20.1% year-over-year.

- Latin America: Estimated revenue of $1.25 billion, suggesting an increase of 8.1% from the prior quarter.

- EMEA: Estimated revenue of $3.3 billion, reflecting an 11.8% rise year-over-year.

- United States and Canada: Estimated revenue of $4.73 billion, indicating a 12.1% increase compared to the previous year.

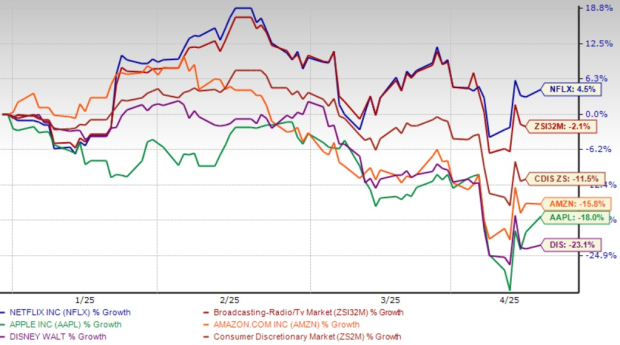

Netflix Stock Performance & Valuation

Year-to-date, Netflix shares have increased by 4.5%. This growth contrasts sharply with notable declines in the Consumer Discretionary sector, as well as dips in stocks of competitors such as Apple (11.5%), Amazon (18%), and Disney (23.1%).

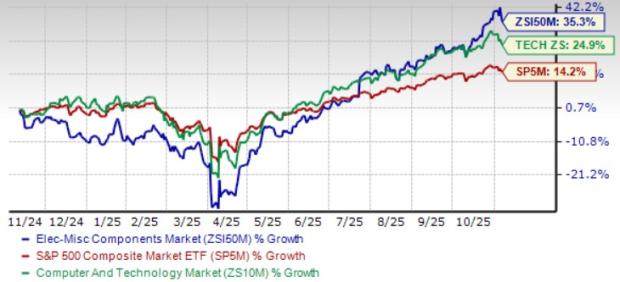

Netflix: Leading the Competition

Image Source: Zacks Investment Research

In summary, while Netflix continues to show resilience and strong growth, investors should approach ahead of the earnings report with caution, considering both the opportunities and challenges that lie ahead.

Netflix Valuation Analysis: Assessing Risks Ahead of Q1 Results

Currently, Netflix (NFLX) trades at 35.4 times its forward 12-month earnings. This valuation exceeds its five-year median of 33.79 times. In comparison, the Zacks Broadcast Radio and Television industry has a lower forward earnings multiple of 25.29 times. As a result, Netflix’s current valuation appears relatively stretched in both historical context and compared to industry peers.

Forward Price-to-Earnings Ratio

Image Source: Zacks Investment Research

Key Considerations for NFLX Investors: Weighing Opportunity and Risk

Netflix continues to showcase robust business fundamentals, highlighted by record subscriber growth, a rich content library, and positive international prospects. Nevertheless, investors are advised to consider maintaining their current positions instead of expanding them at these valuation levels, especially in light of the upcoming first-quarter results in 2025. Although advertising revenues are expected to double by 2025, and operating margins are set to improve to a targeted 29%, much of this anticipated growth seems reflected in the stock price.

Additionally, the company faces potential currency headwinds, a growing competitive landscape, and uncertainty around subscriber retention rates due to recent price hikes. The anticipated return of popular shows and engagement with live sports initiatives promise long-term value creation. Yet, investors may want to exercise patience in seeking a more favorable entry point.

Conclusion: Navigating Netflix’s Current Landscape

The outlook for Netflix remains promising, although the current valuation largely reflects its expected growth trajectory. Given that the first quarter historically experiences seasonal weakness, ongoing currency challenges, and heightened competition, investors should focus on preserving existing positions while awaiting a more opportune entry point. Despite the company’s strength in content and advertising capabilities, a prudent approach may lead to better outcomes as first-quarter results approach.

5 Stocks That Could See 100% Growth

These stocks have been specifically selected by a Zacks expert as top contenders to gain +100% or more in 2024. While past performance is not an indicator of future success, previous stock picks have recorded impressive highs of +143.0%, +175.9%, +498.3%, and +673.0%.

The recommended stocks feature under the radar, presenting an excellent opportunity to invest early.

Discover These 5 Promising Stocks >>

Get 7 Best Stocks for the Next 30 Days—Download Now for Free

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Apple Inc. (AAPL): Free Stock Analysis Report

Netflix, Inc. (NFLX): Free Stock Analysis Report

The Walt Disney Company (DIS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.