All figures are in $CAD unless otherwise noted

All financial information is from Seeking Alpha unless otherwise noted.

Investment Proposition

Nexus Industrial REIT (TSX:NXR.UN:CA)(OTC:EFRTF) has shown relentless aggression in the industrial property acquisition market in recent years. This determined focus has not only expanded Nexus’s portfolio but also streamlined its operations, solidifying its status as a pure-play industrial REIT. From an investment standpoint, Nexus offers a compelling opportunity, characterized by promising rental growth that is expected to surpass its peers, along with an appealing relative valuation. The prospect of decreasing interest rates could further bolster Nexus’s growth trajectory. However, investors should be mindful of potential challenges, including the possibility of a dividend cut and the impact of recessionary pressures in the short term.

Despite these concerns, I am optimistic about Nexus’s ability to navigate these hurdles effectively. For investors with a long-term view, Nexus represents an attractive proposition, combining a robust dividend yield with growth potential, all available at a favorable price point. This blend of income and growth potential positions Nexus as a noteworthy option for those seeking to diversify their investment portfolio in the real estate sector.

Introduction and Property Portfolio

Nexus Industrial REIT, based in Oakville, Ontario, specializes in industrial real estate and boasts a portfolio of 115 properties, spanning an impressive 13.6 million square feet in gross leasable area or GLA. Nexus directly owns approximately 12.1 million square feet, representing 89.11% of the total GLA.

Their diverse property mix includes 84 industrial sites, 16 retail spaces, 13 office buildings, 2 parcels of industrial land marked for redevelopment, and 1 mixed-use facility. All of these assets are located within Canada.

Asset Mix and Geographical Presence

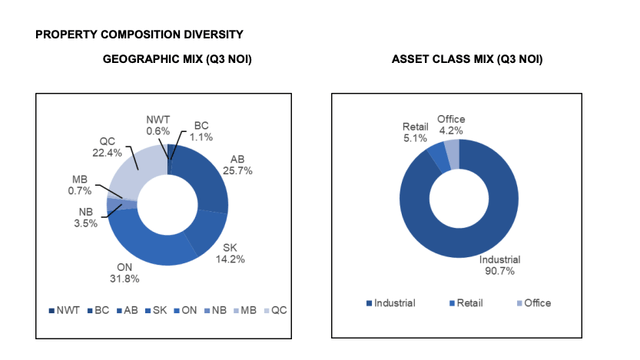

Nexus REIT’s 2023 Q3 financials highlight that their industrial properties are the cornerstone of their business, contributing a significant 90.7% to the net operating income or NOI. Retail and office properties make a smaller impact, contributing 5.1% and 4.2% respectively. Geographically, Ontario leads with 31.8% of the NOI, followed by Alberta at 25.7%, and Quebec City contributing 22.4%. Saskatchewan accounts for 14.2%, while New Brunswick adds 3.5%. The remaining 2.4% is split between British Columbia (1.1%), Manitoba (0.7%), and the Northwest Territories (0.6%).

Nexus Industrial REIT holds a strong tenant profile, with their top 10 tenants accounting for 39.5% of the annualized base rent. This tenant roster includes nationally recognized tenants such as Loblaws (11.8%), Ford (3.9%), and Sobeys (3.4%).

Acquisitions, Dispositions, and Development Activity

Nexus Industrial REIT has shown a high level of activity in the property acquisition market. In the first 3 quarters of 2023, they expanded their portfolio significantly, acquiring five industrial properties for about $322 million, thereby adding approximately 1.43 million square feet to their gross leasable area. In 2022, Nexus spent roughly $317 million acquiring various industrial properties across Canada.

Concurrently, they’ve streamlined their assets by selling two properties including one industrial and one retail property. This aligns with their strategic focus on becoming a purely industrial REIT, as evidenced by their plans to sell four office properties valued at $31.6 million.

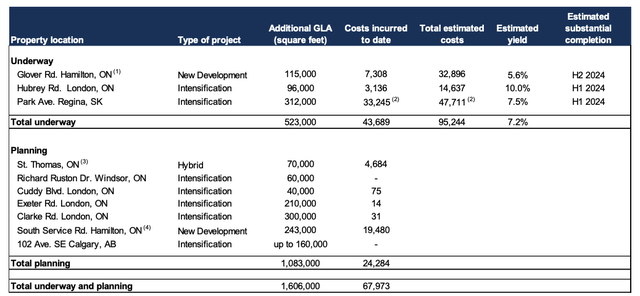

On the development front, Nexus has also been aggressive, investing $42.4 million in various projects during the first three quarters of 2023. They are currently developing an additional 523,000 square feet, with plans for another 1,083,000 square feet in the pipeline. The projects that are currently underway are expected to be completed in 2024 and are anticipated to yield an average return of 7.2%.

Property Metrics and Financials

As of September 30, 2023, Nexus Industrial REIT’s total portfolio boasted a 97% occupancy rate. Breaking it down, the industrial segment led with a 98% occupancy rate, followed by retail at 88%, and office spaces lagging somewhat at 75%.

The lease maturity profile across Nexus’s portfolio is well-staggered. About 11.1% of leases are set to expire in 2024, 13% in 2025, 9.1% in 2026, 4.4% in 2027, and the remaining 60.7% extends from 2028 and beyond. The industrial segment has a weighted average lease term or WALT of 7 years, with the retail and office segments at 3.8 and 4.5 years respectively. Across the entire portfolio, the WALT stands at 6.7 years, favorably aligned with the 5.87-year average term to maturity on their mortgages.

In Q3 2023, Nexus successfully renewed 166,805 square feet of expiring leases at a remarkable rental growth rate of 69% and also managed to lease an additional 15,215 square feet of vacant property. Notably, all new leases incorporate rental steps to help mitigate the impact of inflation.

During the first three quarters of 2023, Nexus realized a fair value adjustment of $60.4 million, reflecting an increase in property values. It’s important to recognize that these are unrealized gains, contributing 38.3% to the year-to-date net income (Author’s calculation). This increase is primarily driven by the growing appeal of industrial properties among investors in Canada. However, I anticipate that this trend might decelerate as we head into 2024.

To conclude our overview of Nexus Industrial REIT, let’s turn to their financing structure, particularly focusing on their mortgage and credit facility obligations. As of September 30, 2023, the weighted average interest rate on their property-secured mortgages stood at 3.31%, a slight increase of just 10 basis points from the year-end 2022 rate of 3.21%. The outstanding mortgage balance is approximately $705 million, with these mortgages having a weighted average term to maturity of 5.87 years. Nexus’s investment properties are valued at $2.26 billion. However, it’s crucial to consider their additional debt from credit facilities, which amounts

Opportunities and Obstacles for Nexus Industrial REIT

Rental Rate Potential

Nexus Industrial REIT is on the brink of a significant upturn in rental revenue, marking a pivotal opportunity for the company. As of September 30, 2023, the average in-place rental rate stood at $9.53 per square foot. However, the estimated market rental rate of $11.91 per square foot indicates a substantial 25% potential increase from the current rates.

A significant portion of this anticipated rental growth is tied to Nexus’s industrial properties in Ontario, where 43.5% of their Gross Leasable Area (GLA) is situated. The expected increases in rental rates in Ontario carry a substantial strategic advantage for Nexus. In particular, Ontario’s market rent is projected to be 47.8% higher than the current in-place rent. While the projected increases in other provinces are more moderate, they are still noteworthy. For instance, Alberta, representing 25.2% of GLA, is expected to see a rental increase spread of 3.1%, while Saskatchewan (15.4% of GLA) is projected to have a spread of 4.1%, and Quebec (10.1% of GLA) a remarkable spread of 42.3%.

Although rental rate growth in Canada has shown signs of slowing due to an increased supply of industrial space, with the growth rate dropping to 11.8% Year over Year (YoY) according to the CBRE report, Nexus remains poised to benefit from these higher rates. In fact, the upturn in rental growth has already yielded positive results for Nexus, with the same property Net Operating Income (NOI) for the year up to Q3 2023 increasing by $2.35 million or 4.1%.

Even with the anticipation of gradual realization of higher market rates, Nexus presents an attractive dividend yield of 7.63%, offering investors a substantial yield while awaiting the projected increases in rental rates. Additionally, Nexus currently offers a Dividend Reinvestment Plan (DRIP) with a 4% discount on shares purchased, further incentivizing long-term investment.

Comparative Valuation

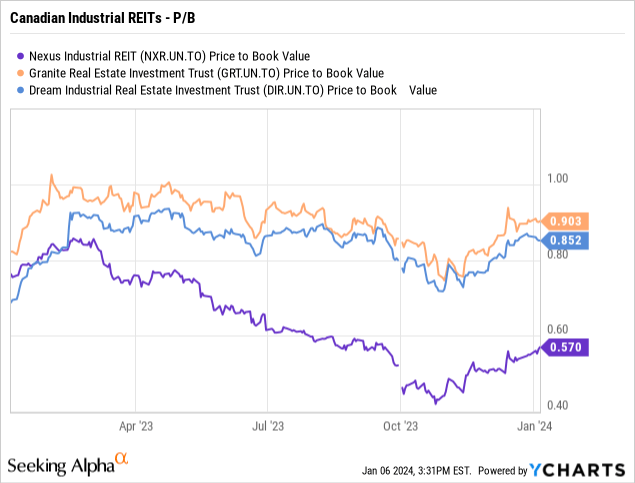

Nexus’s comparative valuation within the industry landscape is a notable point of interest. The company is most closely aligned with Canadian industrial REITs such as Dream Industrial REIT (DIR.UN:CA)(OTC:DREUF) and Granite REIT (GRT.UN:CA)(GRP.UN). Despite the size disparity, with Dream and Granite being significantly larger, Nexus appears to offer substantial value to investors.

Based on the latest analyst estimates from Capital IQ and Seeking Alpha, Nexus is projected to achieve a Funds From Operations (FFO) of $0.8111 per share and an Adjusted Funds From Operations (AFFO) of $0.6788 per share. As of January 5th, 2024, this places Nexus with a favorable P/FFO multiple of 10.34x and a P/AFFO multiple of 12.36x. In contrast, latest figures for Dream and Granite reveal higher multiples, signifying that Nexus is currently trading at substantial discounts – 22.66% for P/FFO and 17.98% for P/AFFO relative to Dream, and steeper discounts of 28.54% for P/FFO and 23.61% for P/AFFO relative to Granite.

While Nexus’s smaller size may warrant a degree of discount, the current gaps in valuation appear to exceed reasonable expectations. Thus, investors are presented with a potential opportunity to acquire Nexus shares at a price below fair value, enhancing the company’s appeal as an investment prospect.

Inherent Risks

Potential Dividend Cut & Dilution

With every investment comes a set of risks, and Nexus Industrial REIT is no exception. One critical consideration is the potential for a dividend cut and dilution. It’s important for prospective investors to recognize that while these risks are significant, they are not exhaustive, and other factors should also be taken into account when evaluating the investment thesis.

Nexus Industrial REIT: Navigating Dividends, Debt, and Economic Shifts

Nexus Industrial REIT has emerged as an intriguing investment opportunity in a financial world fraught with uncertainty. The company’s enviable dividend yield, coupled with its ambitious expansion plans, has captured the attention of astute investors. However, beneath the surface lies a landscape peppered with potential pitfalls – from increasing debt costs to the delicate balance of dividend sustainability. Let’s delve into the multifaceted terrain of Nexus Industrial REIT to discern the potential growth prospects and the lurking risks that investors should carefully contemplate.

Dividend Dilemma: Yield vs. Sustainability

Nexus offers a higher dividend yield compared to its industry peers, which is certainly a positive factor. However, it’s important to address the company’s AFFO dividend payout ratio, which stood at a high 99.1% for the first three quarters of 2023. This marks a noticeable increase from the 92.7% payout ratio at the same point last year, raising some concerns about sustainability.

While the possibility of a dividend cut cannot be entirely dismissed, recent trends suggest a more stable outlook. Specifically, the AFFO payout ratio dropped to 96.1% in Q3 2023, which is lower than the year-to-date average. If this downward trend continues, it would keep the dividend at a more manageable level, although I would prefer to see further reductions for greater confidence. This will be a key aspect to monitor in the fourth quarter of 2023 and throughout 2024.

Additionally, Nexus has expanded its share count significantly, with a weighted average increase of 10.25 million shares from 78.696 million to 88.946 million. This increase is primarily due to the issuance of shares for acquiring new investment properties. While some investors might not see this as a concern, given that the NAV per unit has risen by $0.44 to $12.89, suggesting value-additive deals, there remains a risk. My primary concern is the potential impact on NAV if there’s a reversal in the fair value adjustments of investment properties. Despite the general stability of industrial properties, a 0.25% rise in the capitalization rate could erode property values by $89.3 million. This risk factor, albeit somewhat mitigated, is something that requires careful consideration in Nexus’s overall investment profile.

Higher Interest Rates & Debt Costs

The dramatic increase in interest rates in Canada is not a secret and I believe its full impact on the economy and real estate sector might still be on the horizon, potentially leading to a tumultuous 2024. Nexus Industrial REIT, like many others, is not insulated from these shifts. Nexus has incurred an additional $8.24 million in interest expenses year-to-date as of Q3 2023. However, it’s important to note that this rise is more attributable to an increase in overall debt rather than the hike in interest rates per se. Nevertheless, the prevailing higher interest rate environment could further strain Nexus’s dividend payout ratio.

Assessing Nexus’s debt position, the current debt ratio stands at 48.5%, which I regard as adequate but something that warrants close monitoring. A notable point is that in Q4 2023, Nexus faced the renewal of mortgages amounting to $29.3 million, carrying a weighted average interest rate of 2.36%. It will be important to see how these renewals played out and at what rate were these mortgages renewed.

Nexus has shown a keen awareness of these financial risks. As stated in the outlook section of their MD&A, they are exercising prudence. While committed to completing existing acquisitions and development projects, Nexus plans to be highly selective about new acquisitions until the economic climate shows signs of improvement.

Looking ahead, if interest rates start to decline, Nexus could potentially benefit from the changing landscape. However, in the current uncertain environment, the risks associated with higher interest rates and the broader economic response to these changes are factors that cannot be overlooked. Nexus’s cautious approach in this climate is a prudent strategy, balancing growth ambitions with the need for financial stability.

Conclusion

Key Highlights:

- Growth Potential: Nexus’s robust growth prospects are highlighted by their potential for increased rental revenue, particularly in their industrial segment, which constitutes the majority of their net operating income.

- Attractive Dividend Yield: The REIT offers an appealing dividend yield, which is notably higher than its peers, providing investors with a lucrative income stream.

- Relative Valuation: When compared to industry counterparts like Dream and Granite REITs, Nexus appears undervalued, trading at significant discounts in both P/FFO and P/AFFO multiples.

Risks to Consider:

- High AFFO Payout Ratio: The AFFO dividend payout ratio stands at a high 99.1% for the first three quarters of 2023, up from 92.7% last year. While recent trends indicate a stabilization, the potential for a dividend cut cannot be completely ruled out.

- Share Dilution: The significant increase in share count due to property acquisitions raises concerns about potential NAV impact, especially if there’s a reversal in fair value adjustments of investment properties.

- Higher Interest Rates: Further increases in interest rates as well as recessionary fears could pose issues for debt serviceability.

Therefore, I believe that those with a long-term investment horizon should consider Nexus as the possibility to benefit from a mixture of growth and income could prove beneficial however, investors must consider their own personal goals, risks, and financial situation before making any investment.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.