Market Uncertainty: Key Insights on Zoetis and Investment Strategy

The Stock market is currently navigating heightened uncertainty and volatility due to the Trump Administration’s push to change America’s trade policies. While the market hasn’t plummeted, it has experienced notable losses alongside significant recoveries.

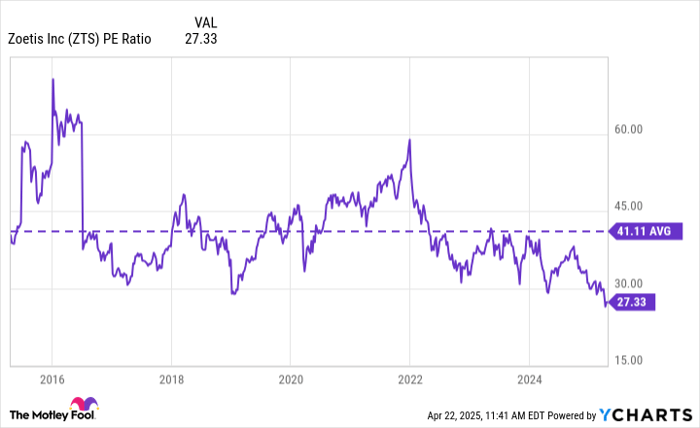

Some stocks, such as Zoetis (NYSE: ZTS), continue to perform well. This stock has averaged a P/E ratio of 41 over the past decade. If a market downturn occurs, investors might find an opportunity to acquire shares at a notable discount.

The Case for Zoetis Investment

Here are reasons for investors to consider Zoetis, especially if the market trends downward.

Leader in Animal Healthcare

Founded from Pfizer’s spin-off of Animal Health in 2012, Zoetis is a prominent player in animal healthcare. The company focuses on medicines, vaccines, diagnostics, genetic tests, and devices for both livestock and pets, boasting annual sales of $9.3 billion.

The demand for animal health products is surging, driven by global population growth and a rising need for animal protein. Moreover, younger generations, particularly in the U.S., are spending significantly more on pets than older generations. A Harris poll highlights that millennials and Gen Z invest more than double annually on their pets compared to Baby Boomers.

Zoetis forecasts the animal health market will expand from $48 billion in 2023 to between $75 billion and $85 billion by 2033. The company is well-regarded in the industry, particularly within companion animals, cattle, and fish segments, and has nearly doubled its annual sales in the last decade.

Strong Dividend Growth Potential

Zoetis offers a compelling dividend strategy, having paid its first dividend in 2013 and increased it annually since. Currently yielding just over 1.3%, the company’s dividend has grown impressively, averaging an annual rate of 21.4% over the last five years.

Although such growth may not last indefinitely, Zoetis is expected to raise its dividend faster than inflation, with a payout ratio at just 33% of 2025 earnings estimates. Analysts predict a long-term earnings growth of 10% per year. While not flashy, consistent dividend increases can lead to substantial wealth accumulation over time, particularly in a stable sector like animal health.

Valuation Challenges Ahead

While it’s clear why Zoetis commands a premium valuation, it’s worth noting that:

- It leads a growing niche market.

- It offers double-digit growth for both business and dividends.

- Current spending trends favor the company.

- It operates in a recession-resistant sector.

However, the stock has been historically expensive, with its P/E ratio averaging over 41 for the past decade. While such premium valuations are common for blue-chip dividend stocks, they seem steep given the projected 10% annual growth rate.

Recent evaluations indicate that Zoetis is trading at a lower valuation of 27 times earnings, yet it still has a PEG ratio of 2.7, suggesting it may not be an immediate bargain. Historically, investments are more favorable with a PEG ratio of up to 2.0 to 2.5. Therefore, the stock might decline further if market volatility persists.

Investment Strategy: Should You Buy Now?

Considering Zoetis’s current valuation, it presents an attractive option for investors. However, gradually purchasing shares while withholding some cash for potential market dips could be wise. Acquiring shares when the P/E ratio falls below 20 could offer significant long-term returns, especially if the stock reverts to its historical averages.

Evaluate Your Investment Approach

Before investing $1,000 in Zoetis, it is essential to consider other options:

The analyst team has identified their 10 best stocks for investment, which do not include Zoetis. These chosen stocks could lead to considerable returns in the near future.

It’s important for investors to assess these opportunities while being mindful of historical performance and market conditions.

Justin Pope has no position in any of the stocks mentioned. The views expressed are solely those of the author.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.