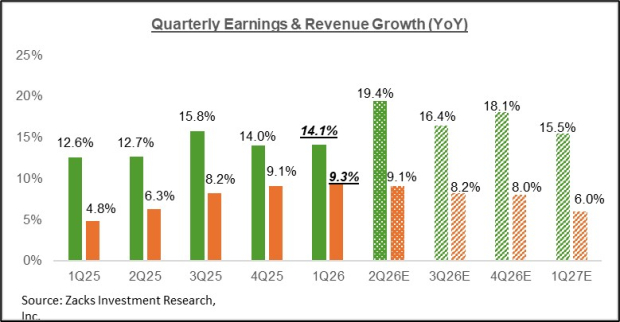

Palo Alto Networks PANW is set to unveil its performance for the second quarter of fiscal 2024 on Feb 2. The company is expected to report revenues in the range of $1.955-$1.985 billion, signifying an 18-20% year-over-year increase.

The Zacks Consensus Estimate for Palo Alto’s revenue is $1.97 billion, predicting a 19.1% growth from the previous year. The company forecasts non-GAAP earnings per share between $1.29 and $1.31, with the consensus estimate pegged at $1.30 per share, implying a 23.8% increase from the year-ago quarter’s earnings of $1.05.

Palo Alto has consistently surpassed the Zacks Consensus Estimate over the past four quarters, with an average surprise of 22.2%. Investors are keen to understand what the upcoming earnings report will reveal about the company’s financial health.

Factors Driving Performance

Analysts anticipate Palo Alto’s robust second-quarter performance to be driven by several factors. The company’s substantial growth momentum from deal wins is expected to bolster its top line. The increasing demand for form factor hardware products and machine learning-powered network security models is likely to have contributed significantly to its quarterly performance.

Additionally, the accelerated shift to the cloud post-pandemic is anticipated to have fueled the adoption of Palo Alto’s platforms. Introduction of cybersecurity solutions in response to rising cyber threats in cloud and remote networks is also expected to provide a substantial revenue boost.

Furthermore, the company’s strategic acquisitions and industry recognitions from the Federal Risk and Authorization Management Program (FedRAMP) are likely to have increased government and public sector adoption of Palo Alto’s products.

Moreover, improved software mix, supply chain efficiencies, and effective cost management are anticipated to positively impact Palo Alto’s gross margin and bottom line in the upcoming release.

Earnings Prediction

Despite the positive outlook, our model does not unequivocally predict an earnings beat for Palo Alto this season. Although the company holds a Zacks Rank of #3, its Earnings ESP stands at 0.00%. As such, it is crucial for investors to closely monitor the upcoming earnings announcement.

Stocks with a Winning Formula

According to our model, companies like NVIDIA NVDA, AutoZone AZO, and Booking Holdings BKNG are positioned to exceed earnings estimates in their impending releases. These firms boast strong combinations of factors that could lead to a positive earnings surprise, making them noteworthy contenders in the market.

NVIDIA, with a Zacks Rank #2 and Earnings ESP of +5.26%, is slated to report its fourth-quarter 2023 results on Feb 21. AutoZone, carrying a Zacks Rank #3 and an Earnings ESP of +3.83%, is expected to announce its second-quarter fiscal 2024 results on Feb 27. Finally, Booking Holdings, with a Zacks Rank #3 and an Earnings ESP of +2.07%, is set to report its fourth-quarter 2023 results on Feb 22.

Interested in staying updated on upcoming earnings announcements? Check out the Zacks Earnings Calendar to track the latest releases in the market.

7 Best Stocks for the Next 30 Days

Experts have identified 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys, deeming these stocks “Most Likely for Early Price Pops.” Since 1988, the full list has outperformed the market by more than 2X, achieving an average gain of +24.0% annually. Therefore, these 7 hand-picked stocks warrant immediate attention.

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

AutoZone, Inc. (AZO) : Free Stock Analysis Report

Palo Alto Networks, Inc. (PANW) : Free Stock Analysis Report

Read the article on Zacks.com for more information.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.