The Current State of PayPal

Over the past 5 years, investors have had a tough time with PayPal Holdings, Inc. (NASDAQ:PYPL) stock: compared to the S&P 500 Index (SP500), which gained 97.31% (total return), the stock has declined ~27% over the period, losing all of its post-pandemic growth in a matter of months:

However, I think that the current state of the company, its renewed approach to future development, the favorable valuation, and the recent technical breakout make PYPL one of the best GARP stocks (growth at a reasonable price) on the market today.

The Growth and Financial Position

PayPal, separated from eBay in 2015, is a global technology platform for digital and mobile payments. It operates in 200+ markets, accepts various currencies, and offers products like PayPal, Venmo, and Braintree for online and offline transactions.

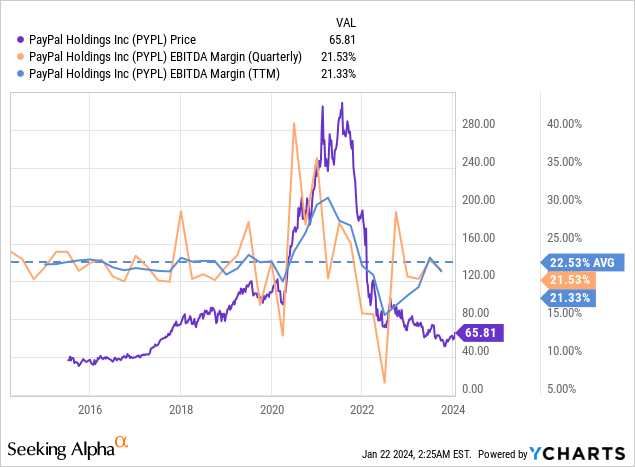

In Q3 2023, PayPal reported adjusted EPS of $1.30, up from $1.08 the previous year, exceeding the consensus of $1.23. Revenues increased by 8% to $7.4 billion (9% FX-adjusted), with adjusted net income rising by 14% to $1.43 billion. Total payment volume grew by 15% to $387.7 billion, contributing to the revenue gain. Active accounts slightly decreased to 428 million. In general, PayPal’s growth rates looked good, and the decline in active accounts was not very dramatic, so the stock didn’t fall further.

Although the company’s margins fell slightly QoQ, they were generally in line with their 10-year average on both a TTM and quarter-on-quarter basis.

In my opinion, this reassured Wall Street analysts, who lowered their revenue growth forecasts due to the projected decline in active accounts but raised their bottom line forecasts (i.e., taking margins into account).

Expanding Reach and Market Strategy

In June 2023, PayPal and KKR announced a multi-year relationship for European buy now, pay later (“BNPL”) receivables, projecting $1.8 billion in proceeds upon closing in H2 FY2023. In my opinion, PayPal will thus further consolidate its position on the already quite stable ground of this rapidly growing market.

Based on the data from Statista Consumer Insights, PayPal is actually the most popular BNPL option in the United States. The company’s interest-free “Pay in 4” option was used by 68% of surveyed BNPL users in the past 12 months. Afterpay comes in 2nd place with a reach of 25.9%, followed closely by Affirm and Klarna.

Change in Leadership and Future Forecast

Having such a large share of such a fast-growing market even while struggling to maintain margins while revenue growth lags behind the rest of the sector is what PayPal has been doing in recent quarters. With the arrival of the new CEO, I, like many legacy (and new) investors, have hope for change.

Why now? Just a few days ago, an interview aired on CNBC with new CEO Alex Chriss, who made it clear that he has a plan. On January 25, 2024, we expect the announcement of a new development strategy for the company which should change the market’s perception of PYPL’s future growth. Alex explained that the company has access to billions of transactions that go through the company on a regular basis. Knowing what worries SMEs and other PYPL customers, the company plans to use AI and leverage all this data to provide a better value proposition.

What I also liked about Alex’s answers was the understanding and awareness that the “former PayPal” spent a lot of time, money, and effort on mergers and acquisitions, losing focus on developing the core operating business. “If it ain’t broke, don’t fix it” – that’s the phrase that came to mind when Alex raised this issue. By trying to pick up growth by a percentage point or two, PayPal has increased its operational risk. Now all the focus is being put on “profitable growth,” according to Alex’s words – that’s exactly what I think was missing before. This is something that should change the game.

As the event on January 25 should be followed by the fourth quarter results release (expected on or about February 1, 2024), let’s take a look at what is priced in for PYPL.

Management’s 4Q FY2023 guidance anticipates 6%-7% revenue growth on a spot basis and 7%-8% on an FX-adjusted basis, with non-GAAP EPS of $1.36, representing 10% growth from the prior year. For FY2023, PayPal forecasts non-GAAP EPS of $4.98 (up from $4.95), reflecting a 21% growth from FY2022. Operating margin improvement is expected to be 75 basis points, as the company is actively reducing its cost structure, targeting at least $1.3 billion in savings for FY2023. The market, in turn, expects faster sales growth and earnings per share in the middle of the management’s guidance range.

PayPal’s Redemption Story: A Strong Buy for 2024

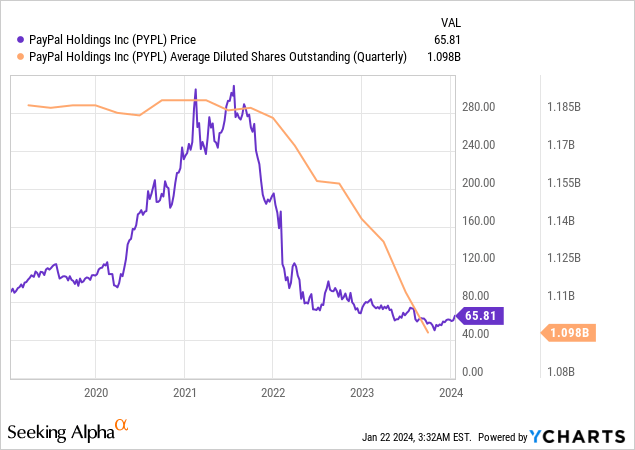

In Q3 2023, PayPal completed a bold move, repurchasing 23 million shares for a striking $1.4 billion. The company now sets its sights on reinvesting its free cash flow (“FCF”) in the business, acquisitions, and buybacks. With an ambitious target of $5 billion in repurchases for FY2023, PayPal is exhibiting an unwavering commitment to reshaping its financial trajectory.

Facts and Figures

To put this into perspective, the $5 billion earmarked for repurchases amounts to approximately 16.9% of fiscal 2023 consensus revenue and around 7% of the total market capitalization. PayPal’s extraordinary ability to generate substantial FCF has enabled the company to buy back roughly 7.6% of its outstanding shares, including stock-based compensation, albeit this has not been adequate in reversing the stock’s recent underperformance.

Looking ahead, an imminent development plan, anticipated to be unveiled on January 25, holds the promise of yielding early fruits as soon as 2024. It is poised to inject new momentum into the growth prospects of PYPL stock, galvanized by the combined influence of buybacks and a recalibrated market perception.

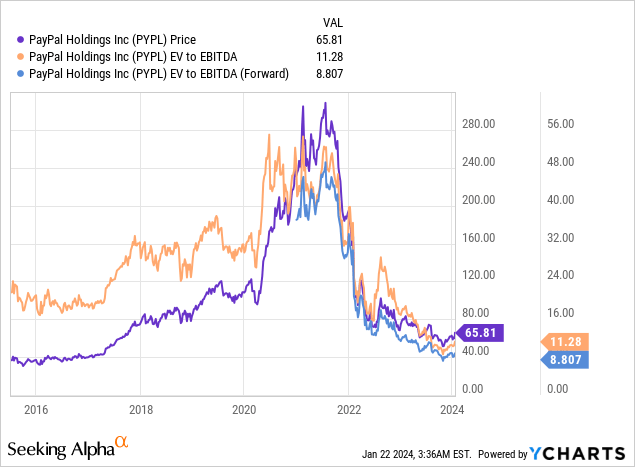

Amid the backdrop of declining revenue growth in recent quarters and the ambiguity swirling around the success of the management’s fresh blueprint, an EV/EBITDA estimate of 15x seems warranted for PayPal, underscoring a departure from its long-term average. Notably, buybacks have a tendency to artificially inflate multiples, a dynamic that must be factored in.

Assuming PayPal achieves $32.1 billion in revenue for FY2024 (reflecting the current consensus estimate) and a full-year EBITDA margin expansion to 25% in light of the cost-cutting measures alluded to earlier, the company’s enterprise value is poised to scale to $120.4 billion. Adapting this figure to the net debt of $11.236 billion portends a tantalizing growth potential of 53.8% come the close of 2024.

Risks To My PayPal Thesis

Venturing into PayPal Holdings Inc. harbors inherent risks, mandating a meticulous evaluation by prospective investors. Foremost among these is market risk, where PYPL’s stock stands vulnerable to broader economic vicissitudes, interest rate fluctuations, and global events, all wielding potential leverage on its stock price.

Within the payments sphere, PayPal contends with fierce competition from stalwart entities such as Apple Pay, Visa’s Checkout, MasterCard’s Masterpass, and American Express’s Later Pay offerings. Additional pressure accrues from digital products peddled by tech behemoths like Meta and Google, culminating in a fiercely contested landscape. The kaleidoscopic array of payment options available at the consumer’s fingertips necessitates PayPal’s continual evolution to stay aligned with ever-evolving consumer preferences.

While PayPal strives to fortify its market stance, the specter of competition and mutable consumer predilections looms large. The company must grapple not only with the imperative of offering paramount convenience and pricing but also pivot to address the burgeoning demand for mobile payment services.

The advent of management transitions introduces another stratum of risk, given that the efficacy of the new leadership cadre in steering through challenges and executing strategic determinations will significantly mold the company’s trajectory and retort to emergent risks. The dexterity of PayPal’s leadership in parrying these fluid market conditions and galvanizing strategic initiatives will be pivotal in shaping the company’s fortunes amidst an intensifying competitive milieu and evolving customer expectations.

Your Takeaway

Despite the expanse of risks enveloping the company, I am inclined to espouse a sanguine outlook. 2024 looms as a harbinger of change, and the forthcoming January 25 disclosure, unveiling the new management’s plan for steering the company’s future trajectory, beckons with anticipation. From every fundamental vantage point, PYPL appears emblematic of a quintessential “Strong Buy”: the market has assimilated the anticipation of sales stagnation, valuation ratios remain subdued, and prospects for additional buybacks and profit-fueled top-line expansion loom on the horizon. What’s not to relish here? Moreover, the technical panorama appears buoyant, with the stock price recently breaching its protracted weekly downtrend line upwards, while the foundational growth potential pinpointed in my valuation analysis aligns squarely with the ensuing logical echelon.

![TrendSpider Software, Oakoff's notes [weekly chart - trendline breakout & 20MA added]](https://static.seekingalpha.com/uploads/2024/1/22/53838465-17059138230882115.png)

Considering the entirety of the foregoing, I pronounce a resounding “Strong Buy” rating for PYPL stock.

Good luck with your investments!

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.