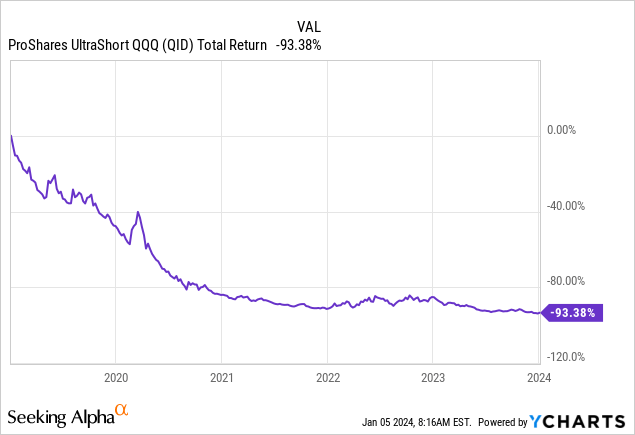

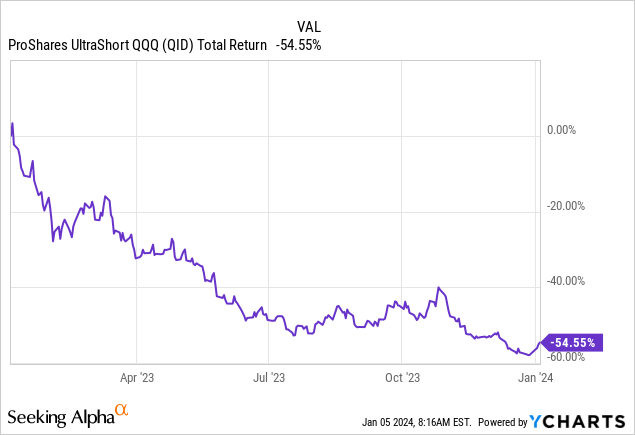

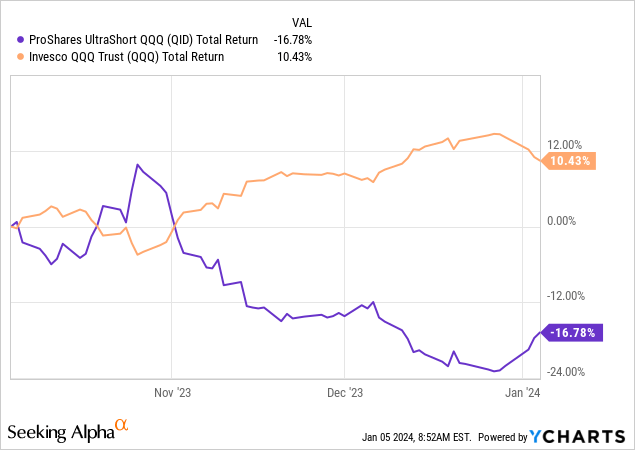

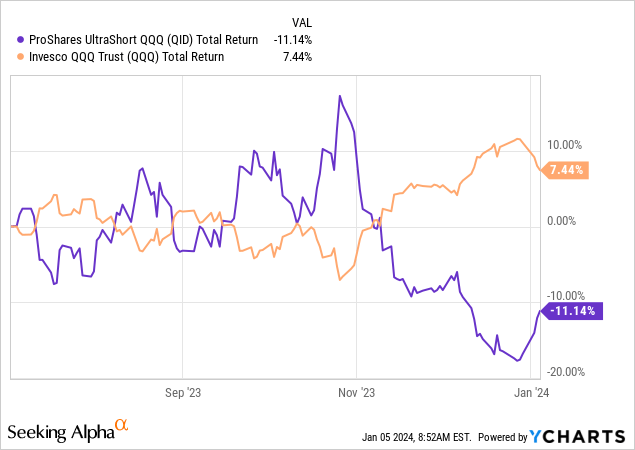

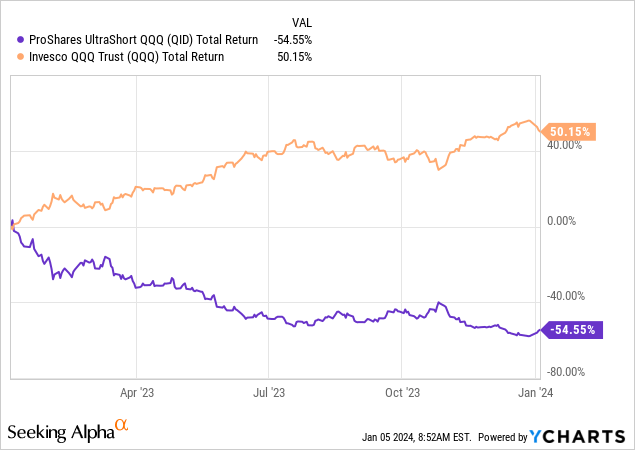

The ProShares UltraShort QQQ ETF (NYSEARCA:QID) has returned -93% over the last five years, in stark contrast to the strong performance of Big Tech stocks through the Invesco QQQ ETF (QQQ). QID, designed to inversely mirror the NASDAQ 100 stocks with 2x leverage, has suffered a significant decline of -54% over the latest 12 months!

Approaching 2024, the potential flip side of such enormous leverage on the wrong side of the market is intriguing. If a recession, especially a deep one, were to occur this year, QID might evolve into one of the top performing holdings in the U.S. ETF universe. Why, you ask?

For starters, U.S. Big Tech names are alarmingly overvalued compared to the broader market and the overall economy. The leading Big Tech stocks, often referred to as the “Magnificent 7”, currently represent a staggering $12 trillion in value out of the total $47 trillion in equity market value listed in New York (Wilshire 5000 index value). This concentration of wealth is unparalleled in American business history.

In the event of a significant recession, bear market, or even a full-blown stock market crash in 2024, QID could swiftly emerge as one of the top-performing investment options. But why make such a claim?

Big Tech stocks are likely to become the major source of liquidity for individuals who have lost jobs during a severe downturn, or for financial institutions seeking to balance escalating losses on their balance sheets and total assets. Panic selling could ensue, where both speculative investors and trend followers in Big Tech hurriedly exit their positions. Dismissing the possibility of this scenario is akin to the blind confidence exhibited by investors in 1929 or the year 2000. Market downturns and crashes are an inherent part of the investment landscape, plain and simple.

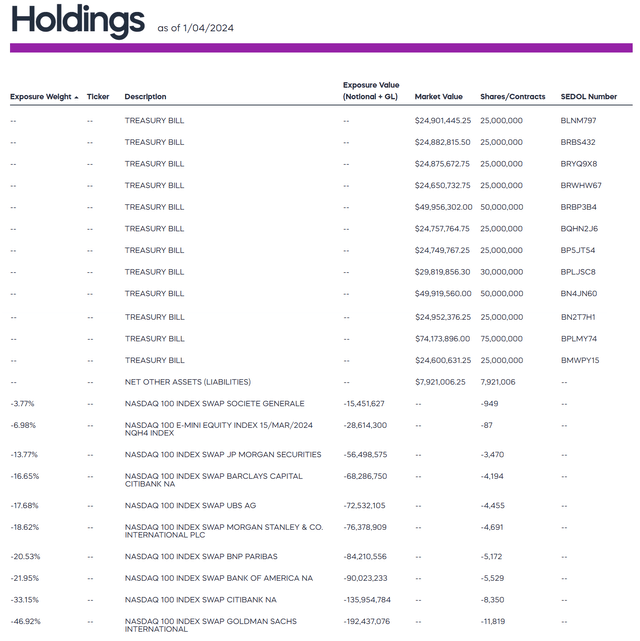

Moreover, the trust design and the substantial earnings from a large cash holding currently yielding over 5% in interest play a crucial role. As of January 4th, 2024, around 93% of net assets were invested in Treasury Bill securities.

In previous years, when interest yields on cash were low, the QID ETF’s 0.95% annual management fee and the costs/premiums associated with rolling over its swap agreements made it exceedingly challenging to achieve its 2x daily rebalance performance goal relative to the NASDAQ 100 index. 2x and 3x ETFs on the short side were notably handicapped, especially in the midst of a bullish market for QQQ-bubble securities.

Surprisingly, the substantial cash yield and lower premiums on swaps have significantly boosted QID returns. The ETF’s trailing 12-month cash dividend payout of 5.3% has not offset the short sale losses from the relentless gains in Big Tech, but the returns over many months have outperformed the 2x design during the 2023 period. If these conditions persist, a substantial decline in QQQ should result in much higher returns than the 2x goal for QID in the near future.

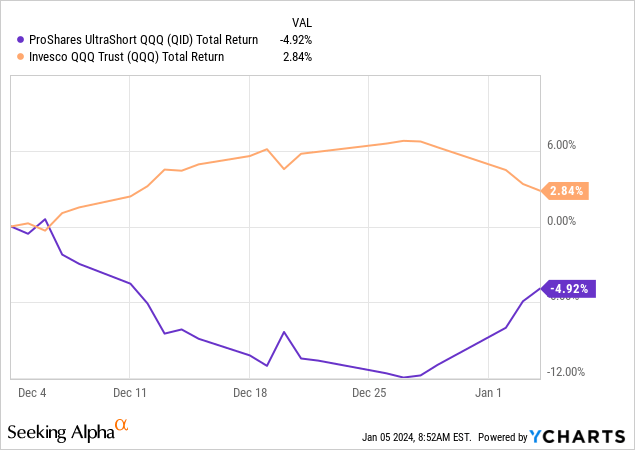

Take a look at the historical performance of QID versus QQQ over the past year to gain a better understanding of the aforementioned points. Remember, traditionally, due to the daily rebalance working against returns over time and the considerable cost of maintaining the 2x leverage, QID used to decrease in value at rates far surpassing the DOUBLE of any QQQ advance since its inception.

Performance in Recessions and Bear Markets

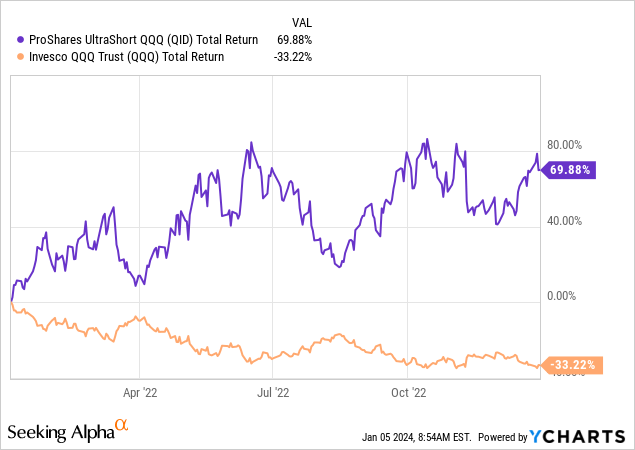

What might the upside potential be for QID holders? One can analyze the total return gains during the 2007-08 Great Financial Crisis, the 2020 COVID-19 pandemic panic, and the 2022 bear market – each resulting in percentage gains exceeding the 2x goal, thanks to the daily rebalance feature that works to compound capital returns to the upside during prolonged trend downturns in QQQ.

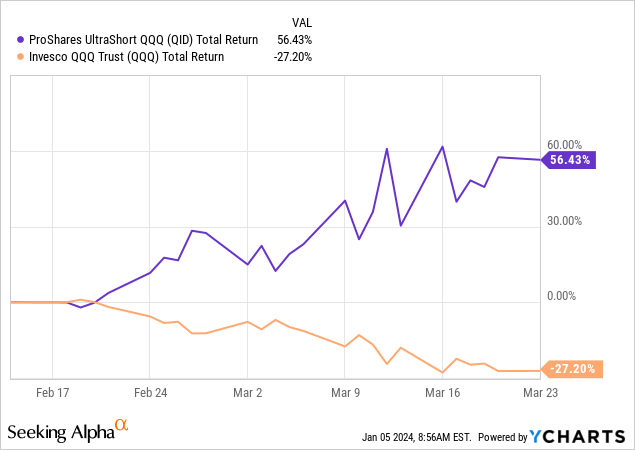

2022 Bear Market

2020 Pandemic Selloff

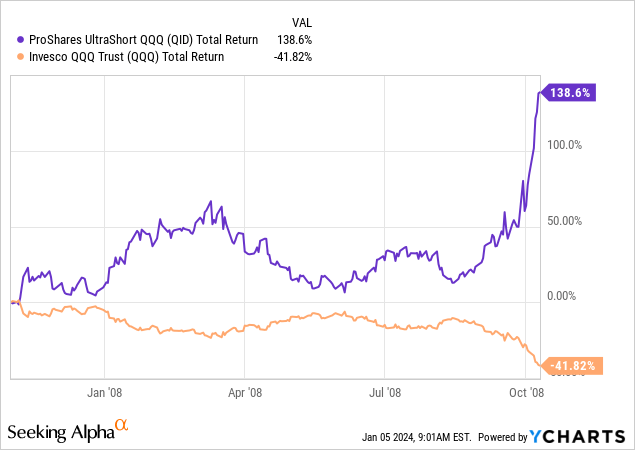

2007-08 Great Recession

Closing Remarks

Given the current advantageous setup for futures/swap contract premiums and unusually high cash yields, it is plausible that any major bearish downturn in Big Tech greater than -20% for a price change could propel QID to deliver a total return of at least +40% (in my estimate), particularly if the move occurs suddenly over a period of less than six months.

Reflecting on the past year of trading in ProShares UltraShort QQQ, it’s challenging to draw any bullish conclusions or extract a promising future for this security. However, there’s undeniable potential for this investment in the event of a major downturn in the Big Tech sector, amplified by the current economic and market conditions.

Exciting Upside Potential for QID ETF in 2024

For investors speculating about a potential economic downturn and the lofty valuations of tech giants, the QID exchange-traded fund (ETF) might just be the underdog surprise of 2024.

Although admittedly a gamble, QID presents a speculative opportunity amidst potential challenging global developments. The risk of holding QID is undeniably high, but the prospects for rewards may materialize in an impending bear market.

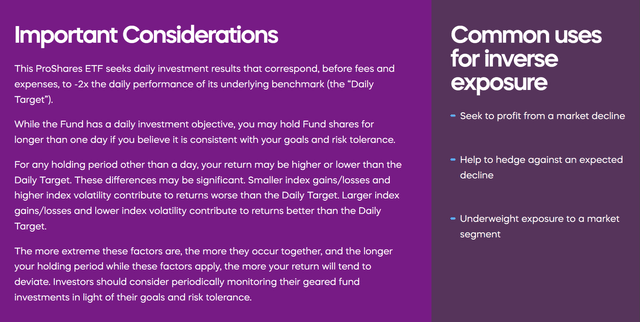

Before diving into this tempting endeavor, it’s essential to consider the unique considerations and risks associated with owning a leveraged inverse ETF like QID, as outlined on the ProShares website.

In many ways, QID finds itself sailing in the same boat as my bullish perspectives on the ProShares Short S&P 500 ETF (SH) and ProShares Short QQQ ETF (PSQ). The two seemingly less-risky 1x products also seem well-positioned, given the current market’s heightened cash yield of 5%+ for shorting the U.S. stock market, in contrast to the meager dividend yields of under 1.5% for holding a regular index fund. Upon extensive research, I have found that QID, SH, and PSQ offer the least expensive downside leverage today, measured against potential rewards, compared to direct shorting or index put options for the average brokerage account.

Should you already possess the leveraged 2x QID ETF, it is imperative to limit your exposure. There exists a fair likelihood of incurring substantial losses, particularly if the general equity market continues its upward trajectory. Personally, I would not allocate more than 1% or 2% of my total portfolio assets to QID. I consider QID a Buy in modest quantities.

As I have reiterated in my prior writings since summer, the valuation of Big Tech giants currently appears overblown and excessively held. In the event of an impending recession this year, I anticipate a prolonged downturn in the pricing of the leading securities of 2023. How one chooses to brace for and engage in such a development remains a discretionary matter.

Thank you for your perusal. Kindly regard this article as your initial step in the due diligence process. It is strongly advised to seek the guidance of a registered and seasoned investment advisor before executing any trades.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.