Robust Growth Prospects Amidst Challenges

DENTSPLY SIRONA XRAY exhibits promise with a strong lineup of products and unwavering commitment to research and development. Yet, foreign exchange fluctuations pose a notable concern.

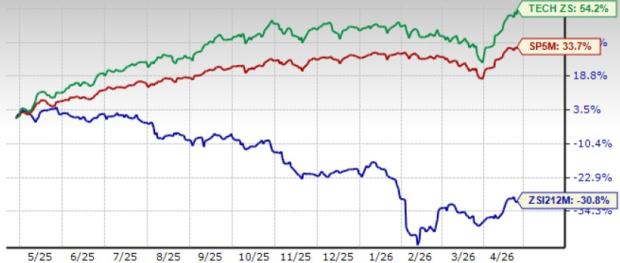

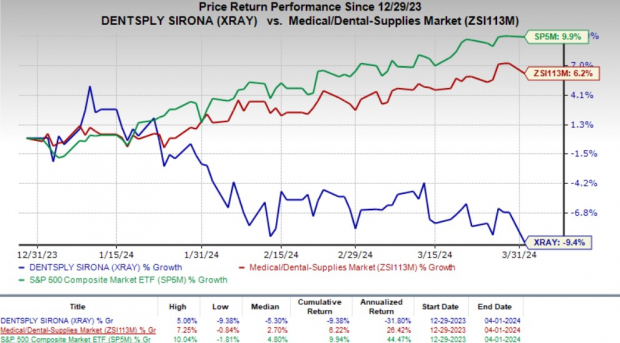

Despite a 9.4% year-to-date decline in shares, this Zacks Rank #3 (Hold) enterprise is distinguished by a market capitalization of $6.88 billion. It boasts global eminence in dental consumables, dental laboratory products, dental specialty products, and consumable medical device products, with anticipated earnings growth of 8.9% over the next five years.

Image Source: Zacks Investment Research

Riding the Crest of Success

The allure of Byte and SureSmile underpins the Orthodontic and Implant Solutions sales for DENTSPLY SIRONA, escalating growth across all regions and product categories via consistent patient footfall and price surges in the Essential Dental Solutions segment. The inclusion of Wellspect Healthcare’s products further bolsters revenue. The surge in aligners and CAD/CAM equipment fortifies sales in Connected Technology Solutions in the fourth quarter.

Moreover, transformational undertakings initiated early in 2023 have yielded fruitful outcomes for XRAY, with workforce streamlining, operational simplification, and decentralized functions driving substantial cost savings. This strategic thrust is propping up the outlook for double-digit earnings expansion in 2024.

Simultaneously, the company is enriching its product array, recently launching the Lucitone for Primeprint and expanding collaborations to elevate the adoption of 3D printing in dental facilities. A dynamic partnership with A-dec underscores the company’s proactive stance in delivering innovative integrated solutions.

Clouds in the Sky

DENTSPLY SIRONA finds itself at odds with macroeconomic turbulences in various regions, especially beyond U.S. borders, dampening sales performance in Connected Technology Solutions due to imaging softness during the fourth quarter. This trend is foreseen to persist through the year. While the U.S. exudes optimism, a gloomy outlook lingers in German and Australian markets, with subdued patient demand in China during the last quarter.

The downturn in sales of equipment, instruments, and implants in the preceding quarter raises red flags for the company.

Analyzing the Future

The Zacks Consensus Estimate for 2024 anticipates revenues to hit $3.99 billion, reflecting a 0.7% uptick from 2023 levels. Adjusted earnings per share are projected at $2.06 for 2024, signaling a 12.5% climb on a year-over-year basis.

Exploring Alternatives

In the broader medical domain, noteworthy contenders like DaVita Inc. DVA, Cardinal Health, Inc. CAH, and Cencora, Inc. COR exhibit potential.

DaVita, bestowed with a Zacks Rank #1 (Strong Buy), showcases a long-term growth rate projection of 12.1%. The company has consistently outperformed earnings estimates, with a remarkable average surprise of 35.6% over the past four quarters. DaVita’s shares have surged 31.6% this year, surpassing the industry’s 9.6% growth.

Cardinal Health, currently holding a Zacks Rank #2 (Buy), is anticipated to experience a long-term growth rate of 14.2%. CAH has exceeded earnings estimates in each of the trailing four quarters, with an average surprise of 15.6%. Cardinal Health’s shares have soared 11.2% this year, outpacing the industry’s 6.2% growth.

Cencora, with a Zacks Rank of 2, projects a long-term growth rate of 9.8%. The company has surpassed earnings estimates in each of the last four quarters, delivering an average surprise of 6.7%. Cencora’s shares have escalated by 18.3% this year, eclipsing the industry’s 6.9% growth.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.