Repsol SA REPYY is set to report fourth-quarter 2023 earnings on Feb 22, before the opening bell.

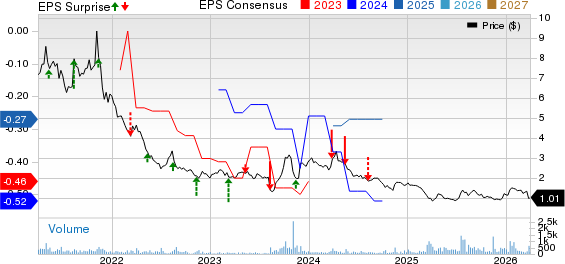

In the last reported quarter, the company’s earnings of 93 cents per share missed the Zacks Consensus Estimate of $1.00. REPYY’s earnings beat the Zacks Consensus Estimate in two of the trailing four quarters and missed the same twice, delivering an average beat of 20.7%. This is depicted in the graph below.

Repsol SA Price and EPS Performance

Repsol SA price-eps-surprise | Repsol SA Quote

Estimate Trend

The Zacks Consensus Estimate for fourth-quarter earnings per share of 80 cents has witnessed no movements over the past 30 days. The estimated figure suggests a significant decline from the year-ago quarter’s reported number.

Factors to Consider

The average spot West Texas Intermediate crude prices per barrel in October, November, and December were $85.64, $77.69, and $71.90, respectively, according to the U.S. Energy Information Administration. Although the prices were not as high as in the year-ago quarter, the commodity prices, higher than the $70 per barrel mark, were impressive and healthy.

Similarly, natural gas prices in the December quarter were also lower year over year.

On the production front, Repsol stated that daily barrels of oil equivalent production in North America and Latin America increased 18.9% and 2%, respectively, year over year.

Thus, although lower commodity prices hurt the integrated firm’s bottom line, higher production is likely to have offset the negative to some extent.

Earnings Whispers

Our proven model does not indicate an earnings beat for Repsol this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. That is not the case here, as you will see below.

Earnings ESP: REPYY’s Earnings ESP is 0.00%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank #2.

Stocks to Consider

Three firms that you may want to consider, as these have the right combination of elements to post an earnings beat this reporting cycle:

Western Midstream Partners LP WES currently has an Earnings ESP of +4.01% and a Zacks Rank #3. The partnership is scheduled to release fourth-quarter earnings on Feb 21.

The Zacks Consensus Estimate for WES’s earnings is pegged at 78 cents per share, suggesting a decline from the year-ago figure.

Cheniere Energy, Inc. LNG currently has an Earnings ESP of +5.55% and a Zacks Rank #3. Cheniere Energy is scheduled to release fourth-quarter earnings on Feb 22.

The Zacks Consensus Estimate for LNG’s earnings is pegged at $2.70 per share.

PBF Energy Inc. PBF has an Earnings ESP of +37.50% and is a Zacks #3 Ranked player at present.

PBF is scheduled to release fourth-quarter results on Feb 15. The Zacks Consensus Estimate for PBF Energy’s earnings is pegged at 8 cents per share, suggesting a massive year-over-year decline.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s credited with a “watershed medical breakthrough” and is developing a bustling pipeline of other projects that could make a world of difference for patients suffering from diseases involving the liver, lungs, and blood. This is a timely investment that you can catch while it emerges from its bear market lows.

It could rival or surpass other recent Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock And 4 Runners Up

Western Midstream Partners, LP (WES) : Free Stock Analysis Report

Cheniere Energy, Inc. (LNG) : Free Stock Analysis Report

Repsol SA (REPYY) : Free Stock Analysis Report

PBF Energy Inc. (PBF) : Free Stock Analysis Report

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.