SoundHound AI’s Revenue Growth Boosts Stock Despite Margin Challenges

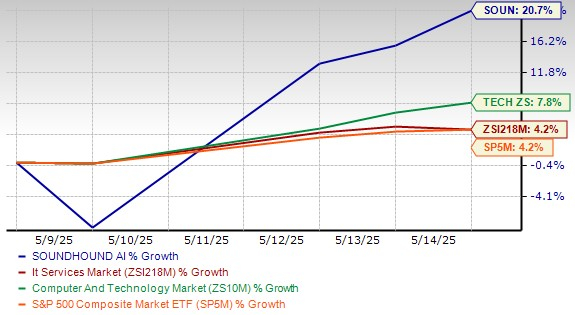

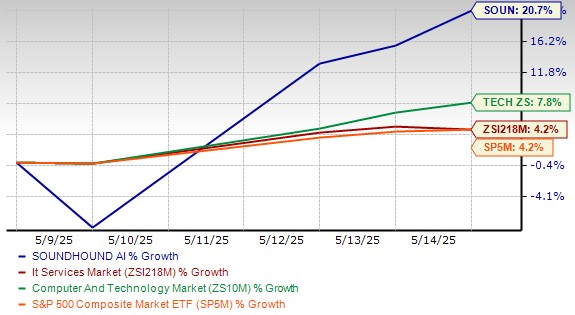

SoundHound AI Inc. (SOUN) has seen its stock price jump 20.7% since reporting its first-quarter 2025 earnings on May 8. This increase outpaces the broader Zacks Computer & Technology sector’s 7.8% gain and the Zacks Computers – IT Services industry’s 4.2% rise. This positive trend reflects heightened investor confidence in the company’s future in the voice AI market.

SOUN’s Post Q1 Share Performance

Image Source: Zacks Investment Research

Highlights from SoundHound’s Q1 Results

In the recent quarter, SoundHound reported revenues of $29.1 million, marking a staggering 151% year-over-year increase. This growth highlights the company’s expanding presence in the voice AI sector. Notably, this revenue figure fell just short of analysts’ expectations, who had forecasted $30 million. On the profitability side, SoundHound recorded an adjusted loss of 6 cents per share, which was better than the Zacks Consensus Estimate of a 7-cent loss. This narrower loss indicates improvements in operational efficiency. However, an adjusted EBITDA loss widened to $22.2 million from $15.4 million, reflecting ongoing investments in growth and research and development.

The company has maintained its revenue guidance for 2025, projecting figures between $157 million and $177 million. If achieved, this would represent an impressive growth rate of approximately 85–109% compared to 2024. This reaffirmation indicates that management is optimistic about sales momentum despite several macroeconomic challenges.

However, SoundHound’s margins faced pressure during this period. The GAAP gross margin dropped to 36.5% from 59.7%, while the non-GAAP margin fell to 50.8% from 65.5%, largely due to rising costs associated with acquisitions and scaling operations. This suggests that operational efficiencies have not yet caught up with revenue growth.

Expanding Customer Base and Market Presence

SoundHound’s impressive revenue growth reflects strong demand for its enterprise AI solutions and a widening footprint in the industry. A key point is the diversification of its customer base, where no single customer accounts for more than 10% of total revenues. This trend underscores the broader acceptance of SoundHound’s voice AI technologies across various sectors, including automotive, healthcare, financial services, and restaurants.

The company’s Polaris multilingual AI model enhances its competitive advantage, featuring superior latency, accuracy, and multilingual capabilities. In Q1, SoundHound activated over 1,000 restaurant locations—nearly ten times its pace from the previous year—and its AI is now managing around 10 million interactions per quarter across 13,000 restaurants.

Strategic Partnerships Enhance SoundHound’s Ecosystem

SoundHound’s collaborations with industry leaders such as NVIDIA (NVDA), Perplexity, Lucid Group, Inc. (LCID), and LG have bolstered its market position. These alliances are crucial for developing innovative voice solutions. The extended partnership with NVIDIA focuses on integrating NVIDIA AI Enterprise tools to elevate SoundHound’s voice AI capabilities. This collaboration promises faster processing, real-time generation, and scalable AI model optimization, already benefiting applications like Lucid Motors’ voice assistant. Moreover, SoundHound plans to further implement NVIDIA AI software in automotive voice technology.

The company’s Q1 success stemmed from rapid expansion across key areas such as restaurants, automotive, and enterprise. Partnerships with Acrelec (restaurant technology), PowerConnect.AI (energy), and Pindrop (security) aim to enhance its market outreach. In automotive, SoundHound is working with Tencent (TCEHY) to incorporate advanced conversational AI into intelligent cockpit systems for global automotive brands, illustrating a growing adoption of its voice commerce solutions.

These partnerships enhance revenue diversification and help the company scale its platform into new markets with minimal incremental costs.

Impact of Recent Acquisitions

SoundHound’s recent acquisitions—SYNQ3, Amelia, and Allset—have contributed significantly to its performance this quarter. These integrations have improved upsell opportunities and expanded technological capabilities. The rollout of Amelia 7.0, powered by SoundHound’s new Agentic Plus framework, allows for the deployment of autonomous AI agents in voice-driven transactions, facilitating real-time applications of agentic AI.

Operational Challenges Affect Profitability

While revenues surged, SoundHound is dealing with margin pressures linked to low-margin contracts and call center operations. The company plans to optimize these aspects within the next 18 to 24 months.

Costs in R&D, Sales & Marketing, and General and Administrative areas surged, increasing by 66%, 117%, and 79%, respectively, year over year. These challenges primarily stem from acquisitions and investments in talent and infrastructure. Although these expenditures are vital for scaling, they impact short-term profitability.

Additionally, automotive volumes faced challenges from geopolitical uncertainties, though an increase in AI-driven average selling prices provided some relief. A transition with a key customer also postponed $2 million in expected revenue from Q1 to later in 2025.

SOUN’s Estimate Revisions

In the past 60 days, the Zacks Consensus Estimate for SOUN’s loss per share for 2025 has held steady at 16 cents, a notable improvement from last year’s loss of $1.04 per share.

Image Source: Zacks Investment Research

Valuation Overview of SOUN Stock

Currently, SOUN shares are considered overvalued, as indicated by a Value Score of F. The forward 12-month price-to-sales (P/S) ratio for SOUN stands at 25.66, which exceeds the Zacks Computers – IT Services industry average of 19.63.

Evaluating SoundHound Stock: Growth Potential and Challenges

Image Source: Zacks Investment Research

SoundHound’s Performance Post-First Quarter

SoundHound experienced a notable 21% stock rally following its first-quarter results, highlighting investor confidence in its long-term growth prospects, particularly in the AI voice-enabled enterprise sector. The company reported remarkable revenue growth of 151%, indicating strong performance across key industries such as restaurants, automotive, and smart devices. Their strategic collaborations with major tech players like NVIDIA and Tencent, along with recent acquisitions, are enhancing SoundHound’s ecosystem and diversifying its revenue sources.

Financial Challenges and Valuation Concerns

Despite these positive indicators, SoundHound faces margin compression and high operating costs, resulting in ongoing EBITDA losses. The firm is forecasting 2025 revenues to reach as high as $177 million. However, the current valuation of SOUN reflects a high forward price-to-sales (P/S) multiple, suggesting that shares may be overpriced. This mixed situation—with significant growth potential countered by operational hurdles and a premium valuation—leads to a Zacks Rank of #3 (Hold). Investors might consider holding SOUN to capitalize on its AI-driven opportunities while awaiting clearer signals of profitability before investing additional funds.

Market Trends and Future Recommendations

Historically, companies in high-growth sectors often face similar balancing acts between growth and profitability. As SoundHound continues to navigate these challenges, its partnerships and revenue growth will be crucial for any future price appreciation. Investors should remain vigilant as they assess the company’s progress and external market influences.

For those interested in exploring stock potential further, analysts suggest a cautious approach until SoundHound shows more consistent profitability signals. Tracking their developments in AI and voice technology may present opportunities in the long run.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.