The reckoning of the technology sector (XLK) has arrived at the outset of 2024’s initial trading week. The nearly impeccable market performance in December 2023 led to a rude awakening for latecomers. The retail FOMO frenzy reached its pinnacle in late December as investors who missed out during Wall Street’s highly pessimistic phase, found themselves compelled to join in.

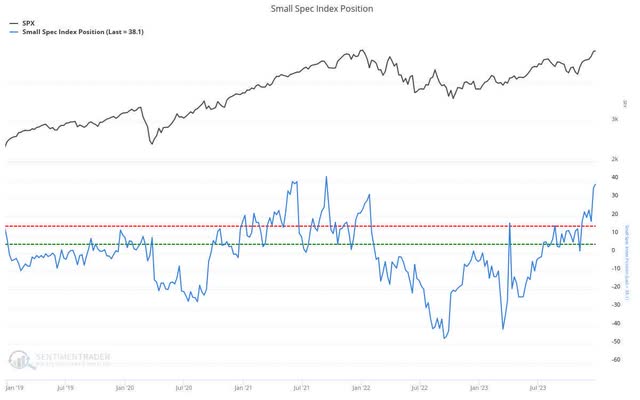

The end of December saw a notably high level of optimism among “small speculators,” non-reportable traders across the market. A sentiment-driven chart reflecting the net position of these small speculators—adjusted for position size and index value, shown in billions of dollars—indicated a surge in bullish sentiment, culminating in frothy levels reminiscent of 2021. In essence, those who chased the December tech rally now face the consequences.

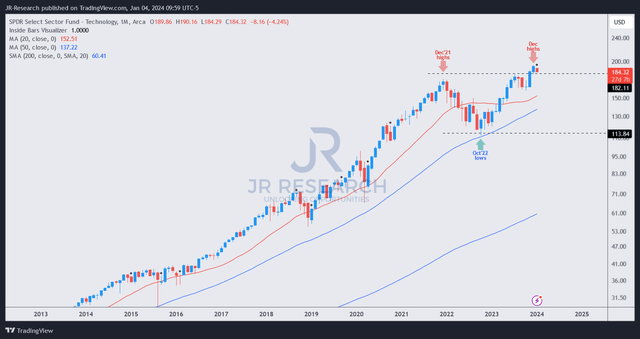

Based on the most recent price action in XLK, most of the gains in December have been erased this week (as of January 4’s trading session). As the chart above depicts XLK’s long-term trajectory, the resolution will only be evident by the end of January. Therefore, although XLK Bulls may argue that it’s premature to conclude ongoing weakness, it reiterates the significance of paying heed to price action and sentiment-driven indicators in assessing risk/reward. Furthermore, the tech sector is currently overvalued by about 5%, based on Morningstar’s sector valuation estimates.

In essence, while the tech sector is indeed overvalued, it falls short of the significantly overvalued levels seen during the pandemic bubble of 2020/21. Nevertheless, the current higher interest rates add a layer of complexity as the market gauges suitable discount rates for tech and growth stocks. This complexity is compounded by uncertainties surrounding the timing of potential Fed rate cuts in 2024. Consequently, investors who adhere strictly to fundamentals are confronted with intricate scenarios that would have been more straightforward had they had a chart to rely on when scrutinizing fundamentally robust stocks.

Personally, I divested from the soaring tech stocks towards the end of December, capitalizing on several opportunities to do so. While I won’t delve into the specifics here out of respect for my members, one thing remains certain: I haven’t been adding to those skyrocketing tech stocks of late. Conversely, the tech stocks I incorporated were those that had been battered to the point of peak pessimism, such as solar stocks.

With this in mind, I present two top stocks for 2024 that, in my opinion, readers should contemplate integrating into their portfolios.

Golden Growth Opportunity

First Solar, Inc. (FSLR) is my preferred avenue to capitalize on the potential resurgence of solar stocks in 2024. Astute investors may recognize that high interest rates, inflated downstream inventory concerns, and an industry-wide demand slowdown dealt a severe blow to solar stocks in 2023. I expounded on the FSLR thesis in early December, outlining why I believe FSLR is well-positioned to spearhead the recovery among its counterparts.

Moreover, FSLR has been awarded an exceptional “A” growth rating and a “B-” valuation grade, indicating a clear dichotomy for a growth stock. The market’s pessimism has spawned a tremendous opportunity for investors astute enough to exploit this division, as FSLR has significantly outperformed the SPX since my mid-December update. I am of the belief that the opportunity is still relatively nascent, as solar stocks could resurge in 2024 as the market re-evaluates the industry post the grueling 2023.

Invaluable Value Find

Investors in the pharmaceutical behemoth, Pfizer Inc. (PFE), embarked on a decade-long rollercoaster in December, plummeting to the pinnacle of pessimism. I previously articulated this in a mid-December update, positing why the market had finally compelled a long-term capitulation. Subsequently, PFE relinquished all its gains from the COVID era and then some, as the market markedly devalued PFE. Evidently, the market seems to have entirely lost faith in its COVID portfolio, prompting investors to hastily flee to avert potential further losses.

Nonetheless, PFE found its floor in December as I had anticipated. Its recent price action indicates that selling pressure has remained containable despite the broad market downturn. As such, I am confident that the market will eventually recognize that Pfizer remains a highly lucrative, wide-moat pharmaceutical company (predicated on an outstanding “A+” profitability grade). Wall Street analysts envision Pfizer’s adjusted EPS growth slump bottoming out this year, and resurging decisively into growth in 2024 (+48% YoY) and 2025 (+24% YoY). These metrics don’t even encompass its long-term portfolio earnings accretion, as they are adjusted EPS growth metrics for the next two years. With an FY25 adjusted EPS multiple of 10.4x (considerably below its 10-year average of 12.9x), the market has likely factored in substantial pessimism regarding Pfizer’s execution in realizing its earnings recovery.

The Bottom Line

With retail investors recently fixated on soaring tech stocks, the ongoing rotation could deliver a harsh reality check to these investors. As individuals keen on potential outperformance, it is imperative to recognize the opportunities present in the market through potential sector or industry rotations well before the broader market catches on.

The two stocks outlined above are ones that my members and I have already seized the opportunity to invest in. I opine that investors looking to pivot their exposure from their hyped tech and growth portfolios should contemplate these two stocks as the prime selections for 2024.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.