WM’s Performance Shows Strong Growth in Waste Management Sector

WM has delivered solid performance over the last year, with its shares climbing 12.9%, surpassing the industry growth of 11.6%. For 2025 and 2026, revenues are projected to grow by 15.9% and 5.4%, respectively, while earnings are expected to increase by 4.8% in 2025 and 12.2% in 2026.

Positive Trends Supporting WM’s Growth

The waste management sector is ripe for expansion. Key drivers include the increasing use of advanced waste collection and recycling techniques, heightened environmental concerns, and industrial growth. Population increases and a rise in non-hazardous waste, fueled by economic development, are opening up new business avenues in this area.

In response to these trends, companies are actively adopting recycling measures for both municipal solid and non-hazardous industrial waste. Additionally, government initiatives aimed at promoting sustainable waste management and reducing greenhouse gas emissions are likely to enhance demand for WM’s services.

WM focuses on core operational strategies that prioritize differentiation and continuous improvement. By enforcing price and cost discipline, the company is positioned to enhance its profit margins. Its long-term growth strategy aims for consistent profitability while efficiently leveraging its assets. Efforts in cost control and process improvement directly contribute to better service delivery.

Investors appreciate WM’s reliable dividend payment history, having distributed $1.21 billion, $1.14 billion, and $1.1 billion in dividends during 2022, 2023, and 2024, respectively. This consistent practice, despite cash flow fluctuations, is likely to retain dividend-seeking investors in the stock.

Challenges Confronting WM

Operating in a competitive landscape, WM faces significant challenges. Local, regional, and national businesses provide stiff competition, particularly municipalities that conduct their own waste collection and disposal operations. These municipalities benefit from tax revenues and tax-exempt financing, posing a threat to WM’s market position. Increased competition may require WM to invest more heavily, potentially affecting its growth and profitability balance.

As of the end of the first quarter of 2025, WM’s current ratio stood at 0.83, below the industry average of 1.04. A current ratio of less than one signals potential difficulties in meeting short-term obligations, raising concerns about the company’s liquidity and long-term financial health.

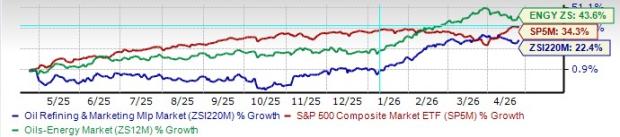

Image Source: Zacks Investment Research

WM’s Zacks Rank & Comparable Stocks

The company currently holds a Zacks Rank #3 (Hold).

Alternative investments within the broader Zacks Business Services sector include Charles River Associates (CRAI) and Duolingo (DUOL), both rated #2 (Buy) by Zacks. CRAI anticipates long-term earnings growth of 16%, having achieved a trailing four-quarter earnings surprise of 19.4% on average.

Meanwhile, Duolingo projects a long-term earnings growth of 44.9% with a trailing four-quarter earnings surprise of 22.8% on average.

Growth Opportunities Ahead

In summary, while WM showcases potential for solid growth amid emerging trends in waste management, it must navigate competitive pressures and liquidity challenges. Investors may want to consider how these dynamics will affect their longer-term strategy.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.