Optimism Surrounds Cousins Properties Amid Growth and Strong Fundamentals

Cousins Properties’ (CUZ) portfolio of Class A office assets is primarily located in the rapidly growing Sun Belt region. Recent trends show a surge in leasing activities as tenants increasingly favor premium office spaces. The company’s effective capital-recycling strategy and strong balance sheet position it well for future opportunities.

Analysts are optimistic about this Zacks Rank #2 (Buy) company. Over the last two months, the Zacks Consensus Estimate for CUZ’s 2025 funds from operations (FFO) per share has risen by 1 cent to $2.79.

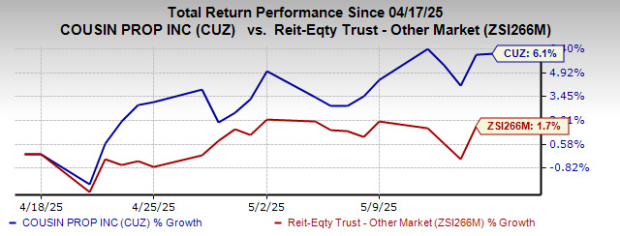

In the past month, shares of this office-based real estate investment trust (REIT) have climbed 6.1%, surpassing the industry’s growth of 1.7%. Given the strong fundamentals, there appears to be potential for further upside.

Image Source: Zacks Investment Research

Key Factors Behind Cousins Properties’ Resilience

Solid Portfolio and Diverse Tenant Base: Cousins Properties boasts an impressive collection of Class A office assets in high-demand Sun Belt markets, which are witnessing a population influx. This region is characterized by strong migration trends and a favorable business climate, leading to increased corporate relocations and demand for office space. Properties in these areas are expected to command higher rents than those in the broader market.

With a significant footprint in the top urban submarkets, Cousins Properties enjoys robust demand for its assets. Its diverse, high-quality tenant roster lessens dependency on any single sector, resulting in stable revenues across different economic cycles.

Healthy Leasing Activity: The company is experiencing strong leasing demand for its top-tier office properties, evident in the rebound in new leasing volume. Continued inbound migration and major investments by tenants expanding their presence in the Sun Belt reinforce this positive trend.

As more tenants return to offices or announce plans to do so, the office market fundamentals in its regions are likely to strengthen.

Capital-Recycling Strategy: Cousins Properties is actively enhancing its portfolio through strategic asset acquisitions and development projects. This capital-recycling approach is expected to support long-term growth, with a notable development pipeline poised to generate significant annualized net operating income in the coming years. By divesting slower-growth assets, the company can redeploy capital toward superior properties in the Sun Belt.

Balance Sheet Strength: Maintaining a solid balance sheet is a priority for Cousins Properties, providing ample liquidity to leverage improving market conditions. Its well-structured debt maturity schedule facilitates access to the unsecured bond market. At the end of Q1 2025, the company held $5.3 million in cash and equivalents, with a credit facility of $38.7 million drawn, leaving an available borrowing capacity of $961.3 million. This strong liquidity offers the flexibility to pursue promising growth opportunities.

Other Noteworthy Stocks

Several other top-rated stocks in the broader REIT sector include CareTrust REIT (CTRE) and W.P. Carey (WPC), both currently holding a Zacks Rank #2. The Zacks Consensus Estimate for CTRE’s 2025 FFO per share is $1.78, projecting year-over-year growth of 18.7%. Meanwhile, WPC’s FFO per share estimate stands at $4.88, predicting an increase of 3.8% compared to the previous year.

Note: Earnings figures mentioned in this article refer to funds from operations (FFO)—a widely adopted metric for assessing REIT performance.

Insights into the Semiconductor Sector

While not the focus of this article, it’s worth noting that global semiconductor manufacturing is forecasted to grow from $452 billion in 2021 to $803 billion by 2028, driven by the rising demand in technologies like Artificial Intelligence, Machine Learning, and the Internet of Things.

The views and opinions expressed herein are solely those of the author and do not reflect those of Nasdaq, Inc.