Market Analysis: Nasdaq-100 Volatility Trends

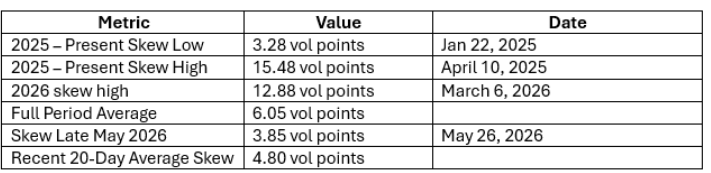

The Nasdaq-100 Index® (NDX®) has seen significant volatility shifts over the past 18 months, marked by emotional responses tracked through the implied volatility (IV) spread between 1-month, 25-delta puts and calls. As of late May, the IV spread fell to 3.94%, nearly the lowest in the dataset, indicating a shift from fear to optimism among investors following a nearly 30% surge in NDX, closing just above 30,000 after multiple all-time highs.

In April 2025, amid tariff-induced market turbulence, the NDX dropped by 20%, prompting the IV spread to expand to around 15.5%, highlighting investor anxiety. However, the index quickly rebounded, fully recovering by summer 2025 as market sentiment stabilized. By late 2025 and into Q1 2026, geopolitical concerns once again raised the IV spread to approximately 13%, despite NDX remaining close to previous highs. This fluctuation reflects changing investor sentiment influenced by macroeconomic factors.

Currently, as investor sentiment tilts towards the upside, those who were previously focused on downside protection are now shifting their strategies, reflecting a broader confidence in the market. This evolving sentiment serves as a critical backdrop for evaluating investment opportunities in NDX options.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.