Study on Nasdaq-100 Option Skew

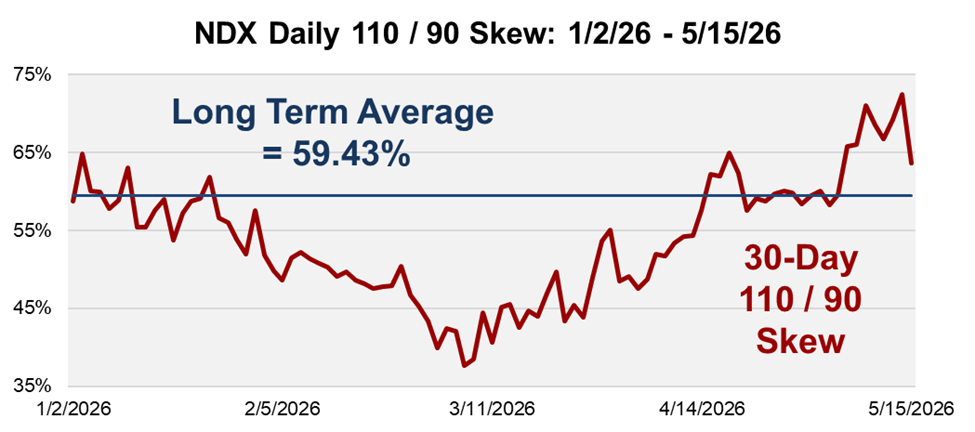

A recent analysis examines whether elevated Nasdaq-100 (NDX) option skew functions as a bullish indicator for market performance. It highlights instances from January 2011 to May 2026 when the 30-day 10% out-of-the-money (OTM) call implied volatility exceeds the corresponding OTM put implied volatility, a condition linked to a “Fear of Missing Out” (FOMO) among traders. Key findings show that the average call implied volatility was 59.43% of the put volatility, with spikes above 70% indicating robust upside demand.

The study assesses NDX returns following days when the NDX 110/90 skew ranked within the top 10% of historical data, revealing notable patterns across various holding periods. Over these periods, averaged returns consistently increased, with a top 1% skew producing an average return of 6.97% over 20 days, indicating that pronounced call skew relates to stronger market performance.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.