Intel’s Stock Sinks as Company Faces Multiple Challenges

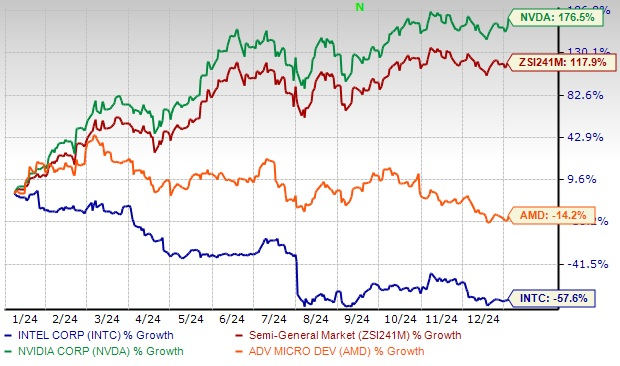

Intel Corporation (INTC) has seen its stock drop by 57.6% over the past year, while the semiconductor industry as a whole has experienced growth of 117.9%. This decline has put Intel behind competitors such as Advanced Micro Devices, Inc. (AMD) and NVIDIA Corporation (NVDA). Analysts blame the company’s poor performance on serious financial difficulties and operational hurdles.

Leadership Change Aims to Revive Intel

In a bid to tackle these issues, Intel has appointed David Zinsner and Michelle Johnston Holthaus as interim Co-CEOs, replacing former CEO Pat Gelsinger. The management team is conducting a thorough review of the company’s operations and is considering options like splitting its product design from manufacturing. One significant plan is to create Intel Foundry as an independent subsidiary, which aims to enhance strategic advantages and improve capital efficiency. The foundry division, however, recorded an operating loss of $5.8 billion in the last quarter.

Intel Trails in Innovation

While other chipmakers adapted to changing market demands, Intel struggled by sticking to its older products. Although Intel made strides in AI chips, it lagged behind NVIDIA, whose H100 and Blackwell GPUs have become hugely popular. Major technology firms have been acquiring NVIDIA’s GPUs to build AI computing clusters, leading to remarkable revenue growth. In contrast, Intel finds itself in a position of playing catch-up.

Additionally, the shift towards AI PCs has strained Intel’s short-term profit margins. The company shifted production to its high-volume facility in Ireland, where costs per wafer are generally higher. Other challenges include higher expenses related to non-essential businesses and an unfavorable product mix, leading to tough margin squeezes.

Intel has also faced difficulties from new competitors in the market, with price wars expected to become fiercer. These pressures could hinder the company’s ability to attract and keep customers, impacting financial outcomes and operational efficiency.

Impact of US-China Relations on Intel’s Profitability

China represented over 27% of Intel’s total revenue in 2023, making it the company’s largest market. However, China’s move to swap U.S.-made chips with local products has negatively influenced Intel’s revenue outlook. The decision to phase out foreign chips from critical telecommunications networks by 2027 highlights China’s push to lessen its dependency on Western technology amid rising tensions with the U.S.

As the U.S. tightens restrictions on high-tech exports, China is also ramping up efforts for self-sufficiency in key industries. This scenario presents Intel with a dual challenge: facing potential market limitations and stiffer competition from local chipmakers. Furthermore, weak consumer spending in China has led to excessive inventory, contributing to soft demand trends. Stringent export controls are expected to exacerbate market conditions, hindering revenue growth in the near term.

Earnings Projections Reflect Market Sentiment

Earnings forecasts for Intel in 2024 have decreased significantly, falling by 106.5% to a projected loss of 9 cents per share. For 2025, estimates have dropped by 55.6% to 92 cents. These revisions indicate a bearish outlook among investors.

Final Thoughts

Intel’s advancements in AI technology have great potential for the semiconductor sector, focusing on scalability, performance, and interoperability, which could facilitate broader AI adoption worldwide. However, with a Zacks Rank of #4 (Sell), it seems that Intel’s recent product introductions may be “too little too late.” Margin pressures due to strict export limitations and poor product mix are likely weighing on profitability. Coupled with plunging earnings estimates and poor stock performance relative to peers, Intel faces a skeptical investor base. Thus, it may not be wise to invest in the stock at this time.

Discover Analyst Picks for Stock Growth

Among thousands of stocks, five Zacks experts each selected their standout pick expected to soar by +100% within months. From these choices, the Director of Research, Sheraz Mian, has identified one stock that is anticipated to have immense potential.

This company caters to millennials and Gen Z, boasting near $1 billion in revenue last quarter alone. A recent decline makes this an opportune moment to invest. Of course, not all elite picks are guaranteed winners, but this particular stock could outperform previous Zacks recommendations, like Nano-X Imaging, which surged by +129.6% in just over nine months.

For the latest recommendations from Zacks Investment Research, explore the list of 5 Stocks Set to Double.

Intel Corporation (INTC): Free Stock Analysis Report

Advanced Micro Devices, Inc. (AMD): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.