Palantir Technologies: Resurgence Fueled by AI Innovations

Data analytics software company Palantir Technologies (NYSE: PLTR) has emerged as a standout performer amid the AI revolution. Since its initial public offering in late 2020, Palantir’s shares have soared, delivering a remarkable 488% return as of market close on November 7.

A Rocky Road to Recovery

The journey for Palantir has not been devoid of hurdles. After a strong debut, the company’s stock struggled in 2022 as broader economic conditions weighed heavily. By the start of 2023, shares traded at a low of $6, which suggested a bleak outlook ahead. The firm’s limited presence in the private sector and declining growth from its government contracts further amplified concerns.

However, the unveiling of the Palantir Artificial Intelligence Platform (AIP) in April 2023 marked a turning point, igniting a resurgence reminiscent of Hollywood’s Rocky Balboa.

Wall Street analysts Dan Ives from Wedbush Securities and Mariana Perez Mora of Bank of America predict price targets for Palantir at $57 and $55, respectively. With AI taking center stage, Palantir’s stock has reached all-time highs, hovering around $56.

Despite the current price leaving limited room for growth compared to analyst projections, it’s crucial for investors to understand the factors driving these upgrades and to consider the potential long-term trajectory for Palantir.

Unprecedented Momentum

In his third-quarter shareholder letter, Palantir CEO Alex Karp boldly stated, “This is still only the beginning.”

This assertive claim comes after the company reported a stellar 30% year-over-year revenue growth, secured over 100 multi-million dollar deals, and generated a positive net income and free cash flow consistently. Typically, one would expect such momentum to taper off at some point.

Nevertheless, Karp, along with Ives and Perez Mora, is optimistic about further growth. An examination of the driving factors behind this enthusiasm reveals a promising landscape for Palantir.

Image source: Getty Images.

Why Are Investors So Optimistic?

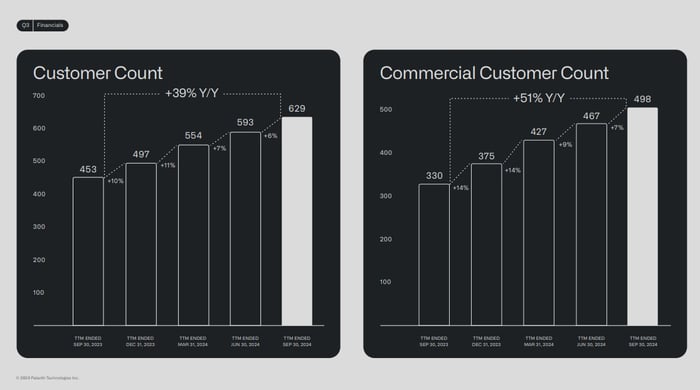

Palantir has distinguished itself by adopting a unique lead generation strategy, welcoming potential clients to immersive seminars known as “boot camps.” These boot camps provide hands-on demonstrations of the software, enabling attendees to explore AI use cases and identify how Palantir can address their challenges.

Image source: Palantir Investor Relations.

The growth figures suggest that these boot camps have effectively expanded Palantir’s customer base while diversifying revenue, particularly with increasing penetration in the private sector.

Importantly, Karp and Wall Street analysts also hint at the untapped potential of Palantir’s government contracts, particularly with the U.S. military’s AI initiatives, which remain critical in the evolving AI landscape.

Strategic partnerships formed this year with industry giants such as Microsoft, Oracle, Meta Platforms, and Amazon still offer significant growth opportunities for the company, although impacts from these alliances are yet to be fully realized.

Should You Consider Investing in Palantir Stock Now?

The benchmark chart below compares Palantir’s price-to-sales (P/S) ratio with other leading software-as-a-service (SaaS) companies. Although Palantir emerges as the most expensive stock in this group, it has experienced considerable valuation growth recently.

PLTR PS Ratio data by YCharts

The momentum behind Palantir’s stock price aligns with the optimistic projections set forth by Ives and Perez Mora. Rather than fixating on current price levels, investors should prioritize understanding Palantir’s strategic growth narrative.

The defense technology sector remains largely untapped, and many collaborations with major tech firms are still in early stages. As customer adoption of AIP increases and new use cases for AI are discovered, the future looks promising for Palantir.

While acknowledging the stock’s current high valuation, I see potential for further gains and agree with the perspective that Palantir’s most exciting phase is just beginning.

Seize a Potential Investment Opportunity

Have you ever felt like you missed a prime investment opportunity? Here’s your chance.

In rare cases, our team of expert analysts issues a “Double Down” stock recommendation for companies poised for growth. If you worry that you’ve missed your moment, now could be the strategic entry point you’ve been waiting for. The numbers speak volumes:

- Amazon: A $1,000 investment when we doubled down in 2010 would be worth $23,446!*

- Apple: A $1,000 investment from 2008 would have grown to $42,982!*

- Netflix: A $1,000 investment made in 2004 would now be worth $428,758!*

Currently, we are issuing “Double Down” alerts on three promising companies, and opportunities like this don’t come along frequently.

See 3 “Double Down” stocks »

*Stock Advisor returns as of November 11, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Bank of America is an advertising partner of Motley Fool Money. Randi Zuckerberg, a former director of market development at Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is also a member of The Motley Fool’s board. Adam Spatacco has investments in Amazon, Meta Platforms, Microsoft, and Palantir Technologies. The Motley Fool holds positions in and endorses Amazon, Bank of America, Datadog, Meta Platforms, Microsoft, MongoDB, Oracle, Palantir Technologies, ServiceNow, and Snowflake. The Motley Fool recommends C3.ai as well as the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.