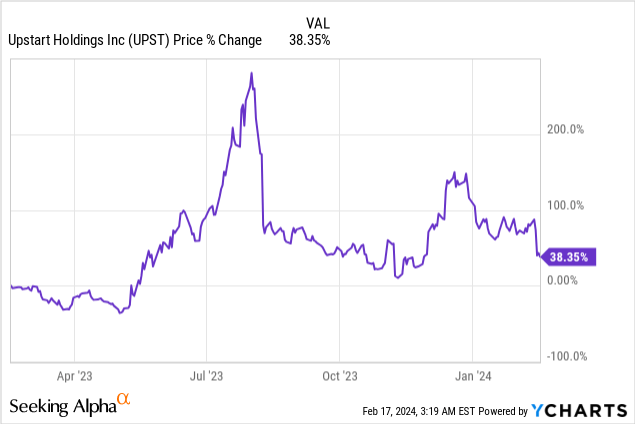

Upstart’s (NASDAQ:UPST) shares suffered a dramatic 20% decline after the Fintech start-up released its fourth-quarter results, outperforming expectations on both the top and bottom lines. However, the AI start-up’s revenue forecast for Q1’24 was viewed as lackluster, falling below consensus estimates. Since Upstart operates as a rate-sensitive credit play for investors, the announcement of the Federal Reserve’s intentions to cut benchmark interest rates in FY 2024 positions the start-up for a surge in loan demand this year. Moreover, with key performance metrics showing improvement, the time is ripe for investors to consider acquiring Upstart shares before the Federal Reserve initiates rate reductions. In my opinion, Upstart’s share value, currently trading below the 1-year average P/S ratio, exhibits strong rebound potential.

Reassessing Previous Rating

In a prior assessment, I deemed Upstart’s shares as a strong buy in November, despite encountering revenue pressures and diminishing loan demand that adversely affected the Fintech’s business. The financial profile of Upstart appears to have further stabilized in the fourth quarter. My belief is that investors are overreacting to the Fintech’s revenue outlook for Q1’24. With the Federal Reserve clearly indicating its intention to pivot its tightening policy in FY 2024, it is only a matter of time until Upstart’s operating fundamentals return to a growth trajectory.

Exceeding Expectations in Q4’23 Earnings

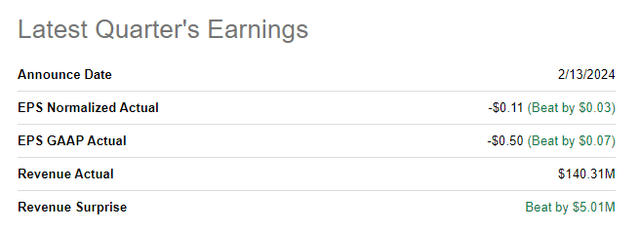

Despite the 20% decline in Upstart’s shares, the Fintech start-up managed to outperform both top and bottom-line estimates in the fourth quarter. Upstart’s adjusted earnings stood at $(0.11) per share, surpassing the consensus of $(0.14) per share. Furthermore, the revenues slightly outperformed, exceeding the consensus by $5M.

Positive Trajectory in Upstart’s Fundamentals

Upstart offers proprietary, cloud-based, AI lending services to its bank partners and charges a fee if a consumer secures a loan through its platform. While primarily focusing on personal loans, the high-interest environment has led to diminished demand for loans.

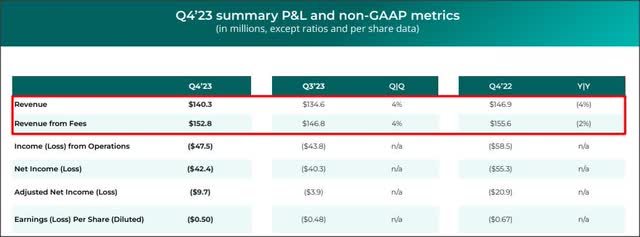

For the fourth quarter, Upstart witnessed a 4% year-over-year decline in revenues to $140.3M, while revenue from fees only decreased by 2% year-over-year to $152.8M. The revenue plunge can be attributed to reduced consumer demand for credit products during high-interest periods. Consequently, most of Upstart’s earnings metrics appeared bleak in the fourth quarter, with a net income of negative $42.4M and an adjusted net income of $(9.7)M. Nonetheless, I anticipate an improvement in these metrics in the latter half of the year, with the Federal Reserve’s plan to lower interest rates potentially boosting demand for loans on Upstart’s AI lending platform.

Enhanced KPIs and Surge in New Loans Quarter-Over-Quarter

While Upstart experienced revenue strain in the fourth quarter, the pressure was not as intense as in the previous quarter when revenues plummeted by 14% year-over-year. Nevertheless, the company exhibited an improvement in key performance metrics such as the percentage of fully automated loans originated and its conversion rate.

Upstart’s credit platform witnessed a 1 percentage point increase quarter-over-quarter in fully automated loans to 89% in Q4’23. Additionally, the conversion rate rose by 2 percentage points from 10% in Q3’23 to 12% in Q4’23.

Ultimately, Upstart represents a credit gamble influenced by interest rates, and I believe the outlook is more optimistic than investors may perceive. As interest rates decline in FY 2024 due to the Federal Reserve’s policy shift, loan demand is expected to rise, making Upstart an appealing growth investment despite the current expensive loan conditions.

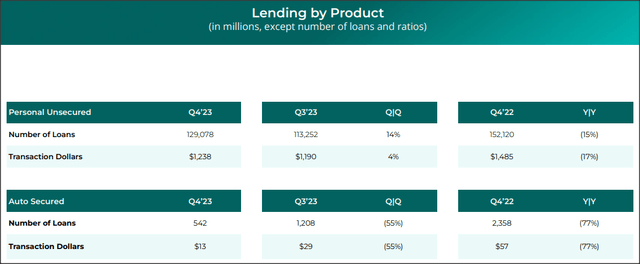

Although loans remain costly at this stage of the rate cycle, Upstart observed a 14% surge in new loans. In the fourth quarter, the total number of loans originated through Upstart’s platform amounted to 129,078, indicating a 14% quarter-over-quarter increase, primarily attributed to the holiday period, which typically drives an upsurge in demand for new personal loans. While Q1’24 may witness a seasonal decline in loan originations and revenues, as indicated by the company’s guidance, the long-term interest rate perspective renders Upstart an attractive growth investment.

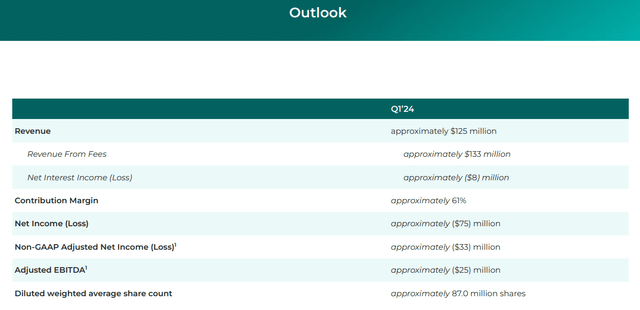

Q1’24 Outlook

Following the earnings release, Upstart shares plummeted by 20%, predominantly due to the below-expectation outlook. The Fintech company projected $125.0M in revenues for Q1’24, while the market anticipated an average top line of $151.3M. This guidance implies an 11% quarter-over-quarter revenue decline. However, I believe the market overreacted to the revenue outlook, as the company’s origination business is poised to receive a significant boost once the Federal Reserve commences lowering interest rates, a move widely expected in the latter half of the year.

Potential Upside for Upstart’s Valuation and Risks Ahead

Valuation Metrics Comparison

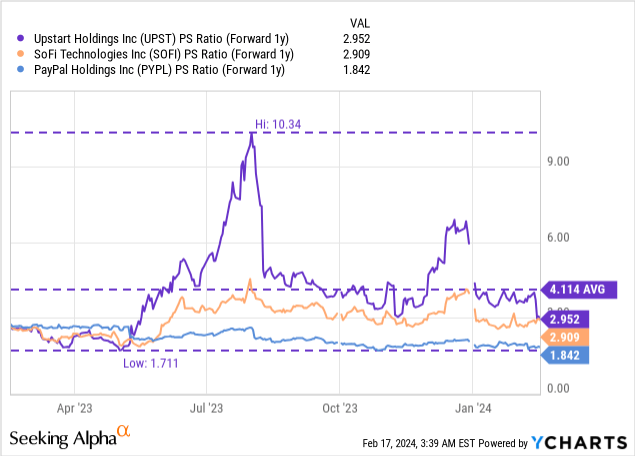

Following a recent sell-off of Upstart, investors may find the current revenue multiplier of 2.95X to be intriguing. This valuation is remarkably similar to SoFi’s 2.95X forward revenues multiple. PayPal, on the other hand, is trading at a lower P/S revenue ratio of 1.84X, partly due to customer-related issues. However, despite market oscillations, Upstart is expected to outpace SoFi and PayPal in revenue growth, with a 31% anticipated increase in FY 2025.

Upstart’s Potential Valuation

Given its robust long-term prospects and a projected 31% revenue growth, a 4.0X revenue multiplier would align more closely with Upstart’s 1-year average P/S ratio of 4.1X. This implies a potential value of $35. As the Fintech’s performance is contingent on interest rate trajectories, this figure remains dynamic.

Potential Risks

The primary risk facing Upstart relates to the Federal Reserve’s intentions to lower benchmark interest rates. A shift in the Fed’s stance, influenced by January’s inflation report, might delay favorable tailwinds for Upstart’s credit business reliant on interest rate fluctuations.

Evaluation of Q4 Performance

Upstart’s Q4 financial report, while reflecting a significant net loss, reveals a less precipitous revenue decline (4%) compared to the prior quarter (14%). This indicates a potential stabilization of the Fintech’s AI-based credit business and improving performance metrics despite negative earnings.

As the second half of FY 2024 is forecasted to witness a decrease in interest rates, there is a potential for Upstart’s credit business to experience a surge in origination as loans become more affordable. Such tailwinds might present an undervaluation opportunity for growth investors with a long-term horizon, especially considering that these future benefits are currently not priced into the stock.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.