Ross Stores Reports Mixed Q4 Results Amid Market Challenges

Dublin, California-based Ross Stores, Inc. (ROST) operates home fashion and off-price retail apparel stores. Boasting a market cap of $47 billion, Ross provides a range of apparel, accessories, footwear, and home items through outlets across the United States.

Performance Overview

The retail giant has slightly underperformed compared to the broader market over the past year. ROST has gained nearly 8% in the last 52 weeks, but has declined by 5.2% year-to-date (YTD). In contrast, the S&P 500 Index ($SPX) has seen 9.2% gains over the same period, with a 3.7% dip noted in 2025.

Industry Comparison

Narrowing the focus further, Ross Stores has also lagged behind the VanEck Retail ETF (RTH), which has surged by 14.3% over the past year and by 2.7% YTD.

Q4 Results and Future Outlook

Ross Stores’ stock rose nearly 2% following the release of mixed Q4 results on March 4. The company reported a 3% year-over-year growth in comparable store sales (comps). However, the previous year’s quarter contained 14 weeks—one week more than the most recent quarter—resulting in a 1.8% year-over-year decline in overall revenue to $5.9 billion, which fell slightly short of Wall Street expectations. Additionally, net earnings saw a 3.8% decline to $586.8 million, although earnings per share (EPS) of $1.79 exceeded consensus estimates by 8.5%.

Despite benefiting from the holiday selling period during Q4, sales have softened since the beginning of 2025, influenced by unseasonable weather and a volatile macro environment. Consequently, Ross Stores anticipates its comps during Q1 2025 will remain flat or decrease up to 3%. Nevertheless, sales may improve in the subsequent quarters.

Fiscal Projections and Analyst Ratings

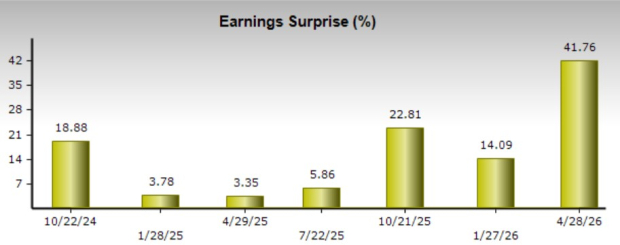

For the current fiscal year ending January 2026, analysts project ROST will achieve a 1.6% year-over-year growth in earnings, reaching $6.42 per share. Notably, the company has a solid earnings surprise history, surpassing bottom-line estimates in each of the past four quarters.

The stock holds a consensus “Strong Buy” rating. Among the 21 analysts covering ROST, there are 16 “Strong Buys” and five “Holds.”

This sentiment is notably more bullish compared to two months ago, when only 14 analysts assigned “Strong Buy” recommendations. On April 8, Wells Fargo (WFC) analyst Ike Boruchow upgraded ROST to “Overweight” and increased the price target from $140 to $150.

Currently, ROST’s mean price target of $160.05 signals an 11.6% premium over current price levels, while the street-high target of $180 suggests a potential upside of 25.5%.

On the date of publication, Aditya Sarawgi did not hold (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article are solely for informational purposes. For more information, please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are solely those of the author and do not necessarily reflect the views of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.