Prologis Reports Q1 Earnings; Stock Shows Mixed Performance

Prologis, Inc. (PLD), the world’s largest logistics real estate investment trust (REIT) with a market cap of $108.7 billion, is based in San Francisco. The company operates modern logistics facilities across 20 countries, managing over 1.3 billion square feet of space.

Over the past 52 weeks, Prologis shares have experienced a slight decline, while the S&P 500 Index ($SPX) has increased by 9.2% during the same timeframe, despite a 3.7% setback this year.

Performance Comparison: Prologis vs. Market

When narrowing the focus, Prologis has underperformed relative to the Real Estate Select Sector SPDR Fund (XLRE), which has gained 11.6% over the last year and 1.7% year-to-date.

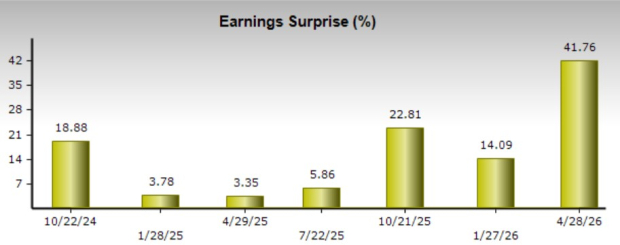

Q1 Earnings Highlights

On April 16, 2025, Prologis announced its Q1 earnings, prompting a 1.8% rise in its stock, as results exceeded analyst forecasts. The company reported revenue of $2.14 billion, reflecting an 8.7% year-over-year increase. Core funds from operations (FFO) stood at $1.42 per share. Operationally, Prologis achieved an impressive 94.9% average occupancy rate across its properties and initiated leases totaling 65.1 million square feet. Additionally, it reported 6.2% growth in cash same-store net operating income, with a notable net effective rent change of 53.7%.

Future Expectations

For the fiscal year ending in December, analysts predict a 2.9% rise in PLD’s core FFO, estimating it will reach $5.72 per share. Historically, Prologis has exceeded consensus earnings estimates in each of the last four quarters.

Analyst Consensus and Price Targets

Among the 24 analysts covering Prologis, the consensus rating is a “Moderate Buy,” based on 13 “Strong Buy” ratings, one “Moderate Buy,” eight “Holds,” and two “Strong Sells.” However, this stance reflects a more cautious outlook compared to the previous month, which had 14 “Strong Buy” ratings.

Baird analyst David Rodgers reiterated an “Outperform” rating for Prologis on May 7, while adjusting the price target from $126 to $120. The average price target is now $119.65, indicating a potential upside of 13.4% from current levels. Moreover, the highest street target of $150 suggests that the stock could appreciate up to 42.2%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information, please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.