Fidelity National Information Services, Inc. (FIS) is experiencing growth, driven by strong Banking Solutions and Capital Market Solutions segments, digital transformation initiatives, partnerships, and solid cash flow that supports shareholder returns.

Fidelity National Information Services: Riding the Wave of Growth

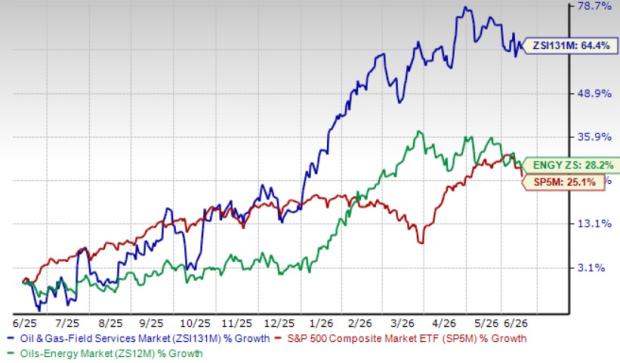

FIS Earnings and Stock Performance

Currently, Fidelity National holds a Zacks Rank of #3 (Hold).

Over the past year, the stock has surged 38.8%, outperforming the industry growth of 24.2%. Additionally, the Zacks Business Services sector rose by 23.3%, while the S&P 500 composite index increased by 28.4% during this time.

Image Source: Zacks Investment Research

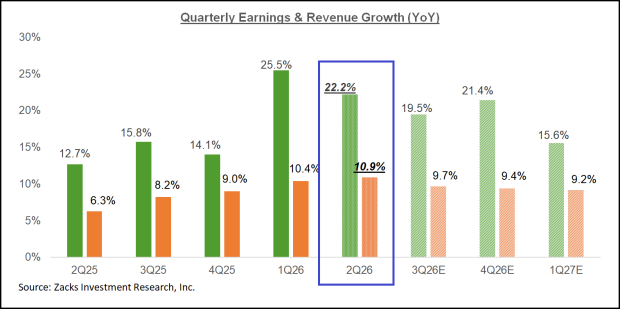

Promising Earnings Growth Ahead

The Zacks Consensus Estimate for FIS’s 2024 earnings stands at $5.18 per share, showing a year-over-year increase of 53.7%. For 2025, earnings are projected to reach $5.72 per share, a 10.4% rise from the 2024 estimate.

Upward Revisions Supporting FIS

In the past 60 days, the Zacks Consensus Estimate for 2024 earnings has been increased by 1.4%.

Consistent Earnings Surprises

Fidelity National has surpassed earnings estimates in three of the last four quarters, with an average surprise of 8.16%.

Business Strengths Fueling Growth

Revenue growth at Fidelity National is propelled by strong performances in the Banking Solutions and Capital Market Solutions segments. While new client acquisitions support the Banking unit, robust sales in the Capital Markets business enhance recurring revenue. FIS primarily earns revenue from U.S.-based clients, but it also maintains a notable international presence in markets like the United Kingdom, Germany, Australia, Brazil, and Canada.

The company strategically combines organic growth initiatives and acquisitions to secure multi-year recurring contracts. Through organic growth activities, FIS focuses on innovating advanced solutions and implementing targeted sales and marketing strategies to attract new clients.

Acquisitions help FIS diversify its product offerings and customer base, extending its reach geographically. Recently, the company partnered with Oracle to enhance utility sector billing and payment solutions by integrating FIS’s BillerIQ on Oracle Cloud Infrastructure.

The current wave of digital transformation represents a substantial opportunity for Fidelity National to utilize its range of technology solutions. The firm continues investing in technological advancements, process efficiencies, and infrastructure enhancements.

With a strong cash position and impressive cash flow generation capabilities, FIS is well-equipped to reinvest in the business and return value to shareholders via share buybacks and dividend distributions. As of September 30, 2024, cash and cash equivalents had tripled compared to the end of 2023. The company generated operating cash flows of $1.4 billion in the first nine months of 2024, marking a 7.1% increase from the same period last year. FIS offers a dividend yield of 1.7%, outperforming the industry average of 0.7%.

Potential Risks for FIS

Despite its strengths, Fidelity National faces challenges, including inflationary pressures that could affect consumer spending and transaction revenues. The ongoing consolidation in the banking and financial services sector may limit revenue growth by reducing the client base. Additionally, a decline in the use of checks impacts FIS’s check warranty and item processing segments, while the shift towards electronic payments raises concerns about fraud. A high debt burden also constrains financial flexibility.

Other Stocks to Explore

Investors may want to consider other well-ranked companies in the Business Services sector, such as ICF International, Inc. (ICFI), RCM Technologies, Inc. (RCMT), and SPS Commerce, Inc. (SPSC). Currently, ICF International holds a Zacks Rank of #1 (Strong Buy), while RCM Technologies and SPS Commerce carry a Zacks Rank of #2 (Buy). You can view the complete list of today’s top Zacks stocks here.

ICF International has consistently surpassed earnings estimates over the last four quarters, achieving an average surprise of 13.56%. The Zacks Consensus Estimate for ICFI’s 2024 earnings suggests a 14.5% increase from 2023 figures, while revenue estimates indicate a 2.8% rise.

RCM Technologies matched or exceeded estimates in two of the last four quarters, with an average surprise of 4.16%. Its 2024 earnings consensus implies an 11.9% improvement from 2023 figures, with revenue expectations suggesting a 5.9% increase.

SPS Commerce has outperformed estimates for the last four quarters with an average surprise of 10.65%. The Zacks Consensus Estimate for SPSC’s 2024 earnings reflects a 21.1% rise compared to 2023, with revenue forecasts indicating an 18.5% increase.

While SPS Commerce stock is up 2.8% over the past year, shares of ICF International and RCM Technologies have experienced declines of 7.1% and 22%, respectively, during the same period.

Investors Eyeing Nuclear Energy Growth

As demand for electricity surges, transitioning away from fossil fuels has become crucial. Nuclear energy is increasingly seen as a viable replacement. Recently, leaders from the U.S. and 21 other nations pledged to triple global nuclear energy capacity. This transition could create significant opportunities for investors in nuclear-related stocks who act promptly.

Nuclear Energy: A Resurgence in Power Generation

Discover Key Players and Stocks in the Nuclear Sector

The report, Atomic Opportunity: Nuclear Energy’s Comeback, examines the major companies and technologies revitalizing the nuclear energy landscape. It highlights three notable stocks that are likely to see significant gains in the industry.

Download your free copy of Atomic Opportunity: Nuclear Energy’s Comeback today.

Fidelity National Information Services, Inc. (FIS): Get your Free Stock Analysis Report

ICF International, Inc. (ICFI): Get your Free Stock Analysis Report

SPS Commerce, Inc. (SPSC): Get your Free Stock Analysis Report

RCM Technologies, Inc. (RCMT): Get your Free Stock Analysis Report

To read the full article on Zacks.com, click here.

The views and opinions expressed herein are those of the author and may not reflect the views of Nasdaq, Inc.