Micron Technology, Inc. (MU) reported record revenues of $41.46 billion for the third quarter of fiscal 2026, a sequential increase of 74% and a year-over-year surge of 346%. The company attributes this growth to robust demand for artificial intelligence (AI) servers and high-bandwidth memory, resulting in a gross margin expansion to 84.9% from 39% a year earlier.

Micron anticipates that DRAM and NAND demand will continue to exceed supply through at least 2027, driven by AI adoption. The company has also signed 16 strategic customer agreements that comprise roughly 20% of DRAM and one-third of NAND volumes. For the upcoming fourth quarter, Micron projects a gross margin of approximately 86%, up from 45.7% last year.

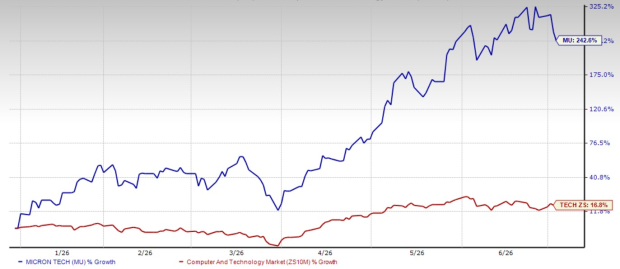

Additionally, Micron’s stock has surged around 242.6% year-to-date, significantly outperforming the Zacks Computer and Technology sector’s return of 16.8%. The forward price-to-earnings ratio for Micron stands at 8.52, compared to the sector’s average of 23.18.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.