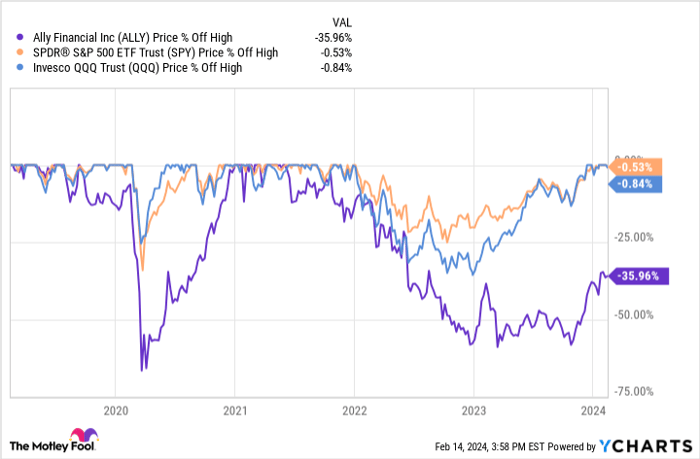

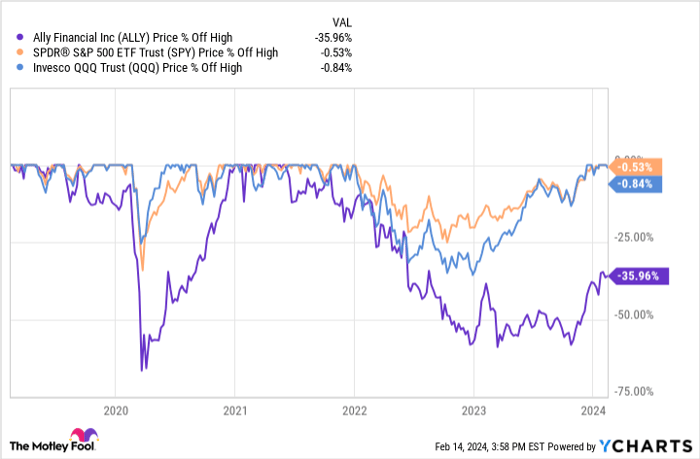

Despite the general market optimism, certain stocks have not soared to the same heights as the broader market. One such stock is Ally Financial (NYSE: ALLY). As the S&P 500 climbs above 5,000 and registers a 5.4% surge in 2024, Ally Financial is still down approximately 36% from its peak, currently at around $36 a share. This slump raises the looming question for investors: is it time to seize this chance and partner with Warren Buffett? Let’s delve deeper into the true value of Ally Financial stock.

ALLY data by YCharts.

Ally Financial: Not Your Legacy Bank

Ally Financial emerged from the aftermath of the 2008 recession when General Motors offloaded its financial arm, GMAC, as part of its bankruptcy recovery strategy. The rebranded entity expanded into a comprehensive consumer bank while retaining its auto loan operations, which still represent over half of its asset portfolio. However, the company’s transition necessitated the development of a new business forte: consumer banking. In a strategic move, Ally metamorphosed into an online-only bank in the smartphone era, enabling it to operate with reduced overhead costs and offer customers attractive interest rates on their accounts.

This strategic maneuver has steered consistent growth, propelling Ally to be acclaimed among the foremost online-only banks in the nation. Boasting $142 billion in retail deposits, 3 million customers, and a steadily expanding customer base, Ally aims to diversify its product offerings, including credit cards, mortgages, and investment opportunities. With only a fraction of the U.S. populace utilizing its services, Ally possesses ample room for expansion, leveraging its proven ability to attract depositors. This augurs well for sustained deposit growth in the years to come.

Higher Interest Rates Aren’t Always Beneficial

The upsurge in the Federal Reserve’s Fed Funds Rate from near 0% in early 2022 to 5.25% in July 2023 posed challenges for Ally as an automotive lender. The rapid interest rate escalation exerted downward pressure on the company’s balance sheet. The confluence of augmenting savings rates for new depositors, declining used car prices affecting borrowing, and increased delinquency in loan repayments accentuated the strains on Ally’s loan portfolio and subsequently diminished its net interest margin from over 4% to 3.2%. However, with the Federal Reserve pausing any further interest rate hikes, Ally anticipates relief from these headwinds, projecting a return to NIM of 3.4%-3.5% by the end of 2024, eventually aiming for a NIM exceeding 4%.

The Stock Appears Undervalued – With a Dash of Patience

In 2023, Ally amassed approximately $1 billion in net earnings, yielding a P/E ratio of nearly 11 based on its market capitalization of $10.9 billion. At first glance, this valuation seems modest. However, the compression of NIM in recent quarters is expected to reverse, fueling the growth of net earnings. Coupled with the consistent expansion of its loan-making resources, Ally could potentially replicate its previous annual earnings of $2 billion, which would notably lower its P/E to around 5. While this endeavor may require time, Ally’s current sub-$40 stock price offers an enticing opportunity for long-term investors.

Should you invest $1,000 in Ally Financial right now?

Before delving into Ally Financial stock, it’s pivotal to consider this: the Motley Fool Stock Advisor analysts recently spotlighted what they believe to be the 10 best stocks for investors to consider, with potential for substantial returns in the ensuing years. While Ally Financial didn’t make the cut, the 10 chosen stocks hold the promise of substantial gains. The Stock Advisor service furnishes investors with a user-friendly blueprint for success, including portfolio construction guidance, analyst updates, and two fresh stock selections each month – all of which have outperformed the S&P 500 since 2002*.

See the 10 stocks

*Stock Advisor returns as of February 12, 2024

Ally is an advertising partner of The Ascent, a Motley Fool company. The author of this article holds no stake in any of the aforementioned stocks. The Motley Fool has positions in and recommends Berkshire Hathaway. The Motley Fool recommends General Motors and recommends the following options: long January 2025 $25 calls on General Motors. The Motley Fool maintains a disclosure policy.

The expressions and opinions articulated in this piece belong to the author and may not represent those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.