UPS Braces for Earnings Reveal Amid Mixed Performance Metrics

Atlanta-based United Parcel Service, Inc. (UPS), the world’s largest express carrier and package delivery company, is set to report its Q3 earnings on Thursday, Oct. 24, before the market opens. Currently, UPS holds a market cap of $115.2 billion and offers a range of services, including transportation, delivery, customs brokerage, and logistics.

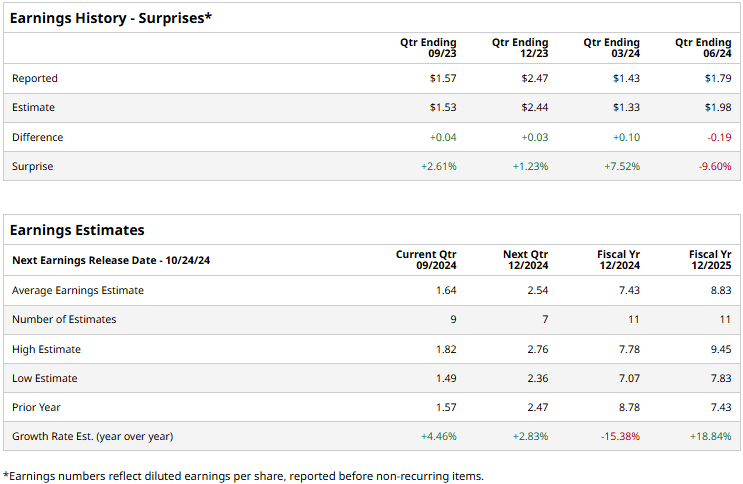

Analysts Project a Modest Profit Increase

As the earnings announcement approaches, analysts anticipate that UPS will post a profit of $1.64 per share, reflecting a 4.5% increase from last year’s $1.57 per share. Over the last four quarters, the company has generally performed well, surpassing Wall Street’s adjusted EPS estimates three times, while missing once. In the last reported quarter, the adjusted EPS fell 29.5% year-over-year to $1.79, which was 9.6% below consensus estimates.

Forecasts for 2024 and Beyond

Looking ahead, expectations for fiscal 2024 suggest an adjusted EPS of $7.43, a decline of 15.4% from $8.78 in fiscal 2023. Nevertheless, analysts are optimistic about fiscal 2025, where the adjusted EPS is projected to rise by 18.8% to $8.83.

Stock Underperformance and Recent Declines

So far this year, UPS has seen its stock price decline by 14.4%, significantly lagging behind the S&P 500 Index’s 21.9% gains and the Industrial Select Sector SPDR Fund’s (XLI) 21.4% returns.

UPS experienced a sharp drop of 12.1% after releasing disappointing Q2 earnings on July 23. The company’s revenues fell 1.1% year-over-year to $21.8 billion, attributed to a 2.6% decline in revenue per piece within its U.S. Domestic segment and a 2.9% dip in average daily volume in the International segment.

Furthermore, UPS reported a 3.1% increase in operating expenses, reaching $19.9 billion. This uptick contributed to a contraction in net margin by 3% compared to last year, dropping to 6.5%, and leading to a significant 32.3% reduction in net income, which amounted to $1.4 billion.

Analysts Hold a Cautious View on UPS Stock

The general consensus on UPS stock remains moderately bullish, reflected in an overall “Moderate Buy” rating. Out of 25 analysts covering the stock, 12 recommend a “Strong Buy,” 12 suggest a “Hold,” and one advises a “Strong Sell.”

The average price target of $144.40 indicates a potential upside of 7.3% based on current levels.

More Stock Market News from Barchart

On the date of publication, Aditya Sarawgi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article are solely for informational purposes. For more information, please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.