Ecolab Set to Release Q3 Earnings: Analysts Predict Strong Growth

Based in Saint Paul, Minnesota, Ecolab Inc. (ECL) focuses on water, hygiene, and infection prevention solutions. With a market cap of $73.2 billion, Ecolab’s services promote safe food handling, clean environments, and efficient water and energy use. The company plans to announce its fiscal Q3 earnings results on Tuesday, Oct. 29, before the market opens.

Expectation of Strong Earnings Growth

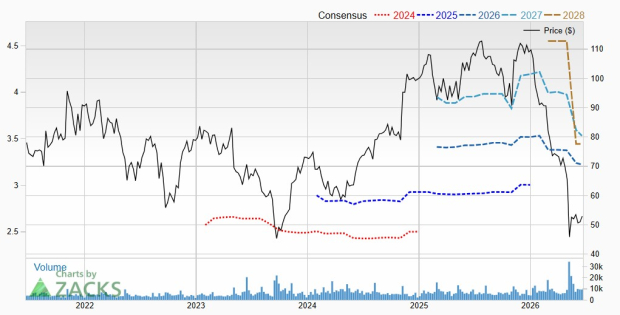

Analysts forecast that Ecolab will report a profit of $1.82 per share for the third quarter, representing an 18.2% increase from $1.54 per share in the same quarter last year. Notably, Ecolab has previously exceeded Wall Street’s earnings projections for four consecutive quarters.

Recent Performance and Growth Drivers

In the most recent quarter, Ecolab achieved adjusted earnings of $1.68 per share, surpassing consensus estimates by 1.2%. Growth in its institutional & specialty and pest elimination divisions, along with an expansion in organic operating income margins, contributed to this success. Lower supply chain costs, value pricing, and increased volume have further supported Ecolab’s growth.

Looking Ahead: Fiscal Year 2024 Expectations

For fiscal 2024, analysts project Ecolab will report an EPS of $6.65, a substantial rise of 27.6% from $5.21 in fiscal 2023.

Stock Performance Outshining Peers

ECL shares have experienced a 31.3% increase year-to-date, outperforming the S&P 500 Index’s ($SPX) 22.5% growth and the Materials Select Sector SPDR Fund’s (XLB) 13.3% return in the same timeframe.

Market Reaction and Analyst Outlook

Despite beating earnings estimates, ECL’s shares fell 7.7% following the Q2 earnings release on July 30. This decline was primarily due to revenue of $3.99 billion missing expectations of $4.03 billion.

Analysts Present a Mixed Perspective

The overall view among analysts is moderately optimistic, giving Ecolab a “Moderate Buy” rating. Out of 25 analysts covering the company, 11 endorse a “Strong Buy,” two recommend a “Moderate Buy,” and 12 suggest a “Hold” rating. This is an improvement compared to three months ago, where only eight analysts favored a “Strong Buy.” The average analyst price target for ECL is $265.95, suggesting a potential upside of 1.8% from current prices.

More Stock Market News from Barchart

On the date of publication, Rashmi Kumari did not hold (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article are solely for informational purposes. Please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.