TTD Shares Face Challenges Amid Economic Uncertainty and Competition

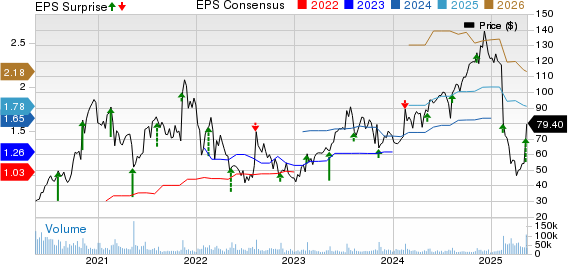

The Trade Desk (TTD) has experienced a 32.5% decline in shares year-to-date. While the company’s first-quarter results exceeded expectations, leading to a 32.6% share increase since May 8, overall revenue growth of 25% indicates solid demand. However, growing economic uncertainty threatens to tighten advertising budgets, which could adversely affect TTD.

Given these conditions, should investors consider adding TTD to their portfolios? This article evaluates the company’s quarterly performance and its long-term outlook.

Q1 Earnings Performance

The Trade Desk reported quarterly revenues of $616 million, marking a 25% increase year-over-year and exceeding management’s guidance of at least $575 million. The adjusted EBITDA reached $208 million, reflecting a 34% margin compared to the $162 million with a 33% margin reported the previous year. Video advertising, including connected TV (CTV), accounted for a significant share of digital spending in the high 40s percentage, with mobile making up a mid-30 percent share. Display ads represented a low double-digit share while audio comprised about 5%. Customer retention remained robust, exceeding 95% for the quarter.

Additionally, TTD showcased net cash from operating activities of $291.4 million and free cash flow of $230 million. Adjusted earnings per share totaled 33 cents, reflecting a 27% improvement from the prior year.

Performance Metrics and New Initiatives

The company also reported significant adoption of its Kokai platform, with two-thirds of its clients utilizing it ahead of schedule. This platform has improved key performance indicators, reporting 24% reduced cost per conversion and 20% lower cost per acquisition. Full client adoption is anticipated by year-end. Management described the integration of Koa AI tools as a “game changer” for the Kokai platform.

Moreover, TTD acquired Sincera, a prominent digital advertising data firm. This acquisition aims to enhance TTD’s programmatic advertising capabilities by incorporating Sincera’s data quality insights. The company’s Unified ID 2.0, which serves as an alternative to third-party cookies, is gaining traction. For the second quarter of 2025, revenues are projected to reach $682 million.

Future Outlook for TTD

The company faces significant challenges due to increasing macroeconomic uncertainty and trade tensions that could compress advertising budgets. TTD has pointed out the ongoing volatility, especially affecting larger global brands. If these macro headwinds continue into the second half of 2025, programmatic demand and revenue growth may further decline.

Intense competition in the digital advertising space, particularly from major industry players like Alphabet (GOOGL) and Amazon (AMZN), adds additional pressures on TTD. Regulatory scrutiny over data privacy and evolving data practices could disrupt existing audience-targeting methods.

Despite CTV being a strong revenue driver, the increasing fragmentation of this market poses risks. TTD’s overwhelming reliance on North America, which accounted for 88% of its revenue, leaves limited opportunities for international growth.

Rising operational costs are likely to impact profitability. In the latest quarter, total operating expenses surged 21.4% year-over-year to $561.6 million, driven by investments in platform capabilities. If revenue growth fails to keep pace with rising costs, profit margins could be adversely affected.

Given these circumstances, analysts remain skeptical about TTD’s stock, evident from revised downward earnings estimates over the last month.

Stock Performance Compared to Peers

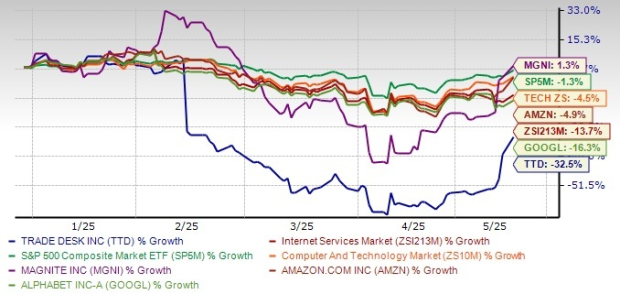

TTD’s 32.5% decline year-to-date surpasses the Internet Services industry’s 13.7% drop and the Zacks S&P 500 composite’s minimal 1.3% decline.

Price Performance

In comparison to its digital advertising peers, including Alphabet and Amazon, TTD has underperformed. Alphabet shares fell 16.3%, while Amazon saw a 4.9% decline during the same period. Conversely, Magnite gained 1.3% year-to-date.

Valuation Concerns for TTD

From a valuation standpoint, TTD appears expensive. The stock is currently trading at a forward 12-month Price/Sales ratio of 12.99, compared to the industry average of 4.75.

Investment Consideration

Despite its strong first-quarter results, The Trade Desk faces considerable challenges from economic uncertainty, increased costs, and fierce competition. Its dependence on CTV and limited international presence further restrict growth potential. The significant stock decline, recent downward earnings revisions, and inflated valuation are compelling reasons for investors to consider selling TTD shares from their portfolios.

For those interested, more detailed insights can be obtained through Zacks’ resources.

The views and opinions expressed herein are solely those of the author and do not necessarily reflect those of Nasdaq, Inc.