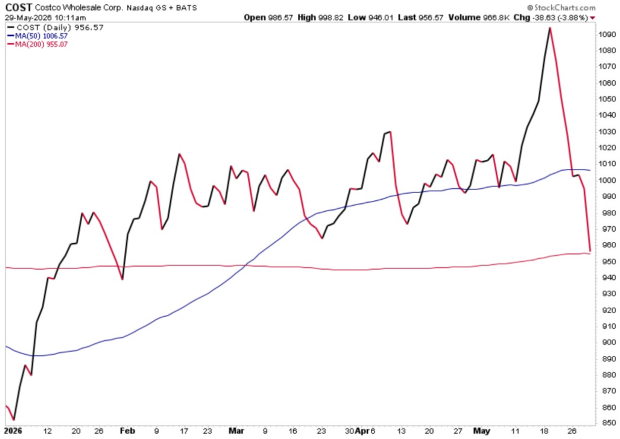

Costco Wholesale reported a strong fiscal third-quarter performance, with adjusted earnings per share (EPS) of $4.93, a 15.2% increase year-over-year, and net sales of $69.2 billion, up 11.6% from $61.96 billion a year earlier. The results, released on Friday, surpassed analyst expectations, with total revenues hitting $70.5 billion, exceeding the consensus estimate of $69.5 billion. Despite this success, Costco’s shares fell approximately 4% in early trading.

Key comparable sales figures show total company comp sales rose 9.8%, driven by 9.4% growth in the U.S., 10.7% in Canada, and 11.2% internationally, while global traffic increased 2.4%. Membership data remains robust, with a worldwide renewal rate of 89.7% and total cardholders reaching 148.5 million, translating to continued growth in high-margin memberships. However, reported gross margins compressed slightly to 11.04%, signaling potential near-term pressure from pricing strategies aimed at maintaining customer loyalty.

Costco’s expansion plans continue, targeting 940 locations by fiscal year-end, and its strong digital growth is now a positive contributor. The ongoing structural advantages—membership economics, supplier leverage, and international growth—position Costco favorably against competitors in the retail space.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.