ExxonMobil: High Valuation Amid Promising Prospects

Exxon Mobil Corporation (XOM) is currently viewed as pricey compared to its peers, trading at a trailing 12-month Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization (EV/EBITDA) of 6.95x. This is significantly higher than the industry average of 4.28x. Generally, a premium valuation indicates confidence in a company’s future performance.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Yet, this elevated valuation requires a closer look at the fundamentals, growth opportunities, and overall market context surrounding the company.

Driving Growth Through Permian & Guyana

ExxonMobil is making strides in the Permian Basin, having acquired Pioneer Natural Resources Company on May 3. The merger results in a sizable portfolio with 1.4 million net acres in the Delaware and Midland basins, estimated at 16 billion barrels of oil equivalent. This acquisition significantly boosts ExxonMobil’s upstream capabilities.

Company projections indicate that, based on 2023 production volumes, output from the Permian will more than double to 1.3 million barrels of oil equivalent per day (MMBoE/D). Furthermore, they expect to reach 2 MMBoE/D by 2027.

In addition to the Permian, ExxonMobil has a strong project pipeline in offshore Guyana. The company stands to gain significant returns from both regions due to low production costs. Favorable oil prices this year should lead to notable cash flows from their upstream operations, which are the primary contributors to overall earnings.

ExxonMobil’s Integrated Approach and Financial Stability

ExxonMobil’s integrated business model offers resilience against falling oil prices. Its operations span exploration, production, refining, and chemicals, providing a buffer during economic downturns.

The company’s balance sheet shows strength; it maintains a debt-to-capitalization ratio of 13.34%, relatively lower than the industry average of 22.38%. Favorable commodity prices have improved its financial standing, allowing for debt repayments incurred during the pandemic.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Chemical Corporation (CVX) also boasts a strong balance sheet, with a slightly higher debt-to-capitalization ratio of 14.13%. BP plc (BP), another major player, is actively reducing its debt amidst rising oil prices and lower capital expenditures, though it still has a substantial debt-to-capitalization ratio of 41.82%.

ExxonMobil’s New Ventures: Lithium, LNG & Carbon Growth

ExxonMobil is diversifying by tapping into the lithium market, which is vital for electric vehicle (EV) batteries. As global demand for lithium escalates, ExxonMobil is well-positioned to leverage this trend. Additionally, the company’s liquefied natural gas (LNG) initiatives, including the Golden Pass and Qatar expansions, along with ambitious carbon capture projects, offer significant growth opportunities. These advances will bolster ExxonMobil’s competitive positioning in the evolving energy market.

Does XOM’s High Valuation Reflect Its Fundamentals?

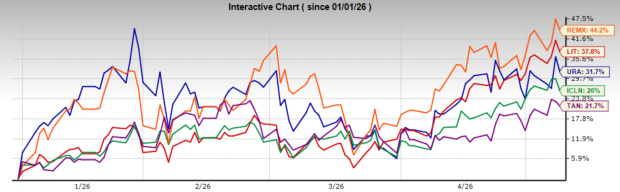

Investors have priced in a premium for ExxonMobil, fueled by expectations of strong growth and profitability in the future. Year-to-date, XOM has appreciated by 20.7%, outpacing the industry’s average increase of 11.8%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

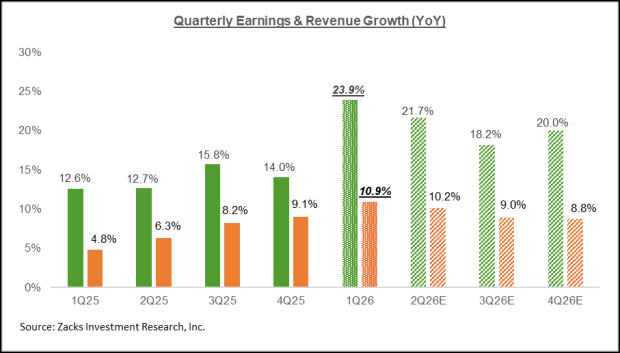

Notably, challenges persist, such as declining refining margins and a sharp decline—nearly 60%—in year-to-date earnings from Energy Products, as reported with the third-quarter 2024 results. This underscores the inherent risks facing ExxonMobil.

With the majority of its earnings stemming from upstream activities, volatility in oil and gas prices poses significant risks to the company’s overall performance. Thus, while XOM’s long-term outlook remains bright, caution is recommended for investors. Holding a Zacks Rank #3 (Hold), it may be wise to await a more favorable entry point before adding XOM to their portfolios.

Free Resources: 5 Stocks to Buy Amid Infrastructure Investment

Trillions in Federal funding are allocated to enhance America’s infrastructure. This investment will not only enhance roads and bridges but also boost renewable energy and data centers.

Explore 5 surprising stocks that are well-positioned to benefit from this growing investment landscape.

Download the “How to Profit from the Trillion-Dollar Infrastructure Boom” report for free today.

BP p.l.c. (BP): Free Stock Analysis Report

Chevron Corporation (CVX): Free Stock Analysis Report

Exxon Mobil Corporation (XOM): Free Stock Analysis Report

Read this article on Zacks.com.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.