Challenges Plaguing CBRL

The echoes of a tempestuous year in 2023 continue to reverberate through the hallowed halls of Cracker Barrel Old Country Store, Inc. (CBRL), leaving the company grappling with fierce headwinds. Forces such as inflation in commodity prices and wages, alongside plummeting comparable store retail sales, cast a shadow on their path to prosperity.

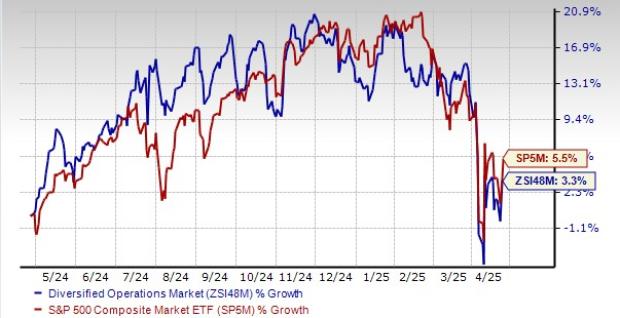

Over the past three months, CBRL stocks have weathered a 16.5% decline, a stark contrast against the formidable growth of 7% in the S&P 500 and the 1.5% rise in the Zacks Retail – Restaurants industry. The gloom continues to loom large as analysts have downsized fiscal year 2024 earnings estimates from $4.78 to $4.62 per share in the last thirty days. With the Zacks Consensus Estimate projecting a 15.5% dip in CBRL’s fiscal 2024 EPS compared to the previous year, the disquiet among market-watchers grows.

Image Source: Zacks Investment Research

Factors Stunting Growth

Cracker Barrel finds itself ensnared in a web of inflationary pressures, constraining operational performance and chipping away at profit margins in recent quarters. Despite deploying cost-saving measures, the company continues to grapple with escalating labor costs fueled by augmented wages and boosted investments in additional labor hours, likely to keep profit margins under siege consistently.

The tale of woe continues as during the second quarter of fiscal 2024, comparable store retail sales took a gut-wrenching plunge of 5.3% year-over-year. A somber symphony of declines echoed across most categories, with toys, food, and decor bearing the brunt of the downturn.

The quarter saw a 130 basis points downturn in the total cost of goods sold as a percentage of total revenues, settling at 33.7%. Even though the total cost of goods saw a dip year-over-year, labor costs, alongside other store operating expenses, witnessed an upward trajectory, climbing 90 bps to 34.5% and 50 bps to 22.9%, respectively. The surge in labor and other related expenditures was spurred by investments in additional labor hours to bolster the guest experience and a 5.4% hike in hourly wage inflation.

Alas, the adjusted operating margin for the quarter stumbled to 3.8%, a fall from the 4.5% reported in the year-ago quarter. The downtick primarily stemmed from a surge in labor and related expenses, other operating costs, and general administrative expenses. Surveying the quarterly landscape, CBRL predicts a dwindling third-quarter adjusted operating income compared to the preceding year.

While the quarter bore witness to robust sales and an uplifting 300 basis points surge in traffic trends compared to the first quarter, the acknowledgment of operating in an uncertain climate is a sobering note. Lingering challenges continue to mar the industry’s landscape, with CBRL anticipating a persisting pressure on industry traffic for the remainder of the fiscal year.

Top Choices

For investors seeking calmer waters in the retail segment, sunnier prospects shimmer over the horizon:

Brinker International, Inc. (EAT) stands tall with a Zacks Rank #2 (Buy). Surging ahead with a trailing four-quarter earnings surprise averaging 212.7%, EAT stocks have shimmered with a 31.9% surge in the past year. The fortunes seem bright, with the Zacks Consensus Estimate for EAT’s 2024 sales and EPS projecting a 4.9% and a staggering 30.4% growth, respectively, from the previous year.

Texas Roadhouse, Inc. (TXRH) takes center stage with a Zacks Rank #2. Not without its share of turbulence, raking in a trailing four-quarter negative earnings surprise of 3.9% on average, the stock still charts a 43.3% ascent over the past year. Forecasts unveil a promising uptick with the Zacks Consensus Estimate envisioning a 14.1% rise in 2024 sales and a 25.8% growth in EPS from the prior year.

Shake Shack Inc. (SHAK) struts in with a Zacks Rank #2 and a dazzling trailing four-quarter average earnings surprise of 92.6%. The stocks sparkle, reflecting an 87.2% surge in the past year. A bullish outlook persists with the Zacks Consensus Estimate predicting a 14.6% sales hike and a striking 91.9% rise in EPS for 2024 from the previous year.

Infrastructure Stock Boom to Sweep America

A massive push to rebuild the crumbling U.S. infrastructure will soon be underway. It’s bipartisan, urgent, and inevitable. Trillions will be spent. Fortunes will be made.

The only question is, “Will you get into the right stocks early when their growth potential is greatest?”

Zacks has released a Special Report to help you do just that, available for free today. Discover 5 special companies poised to gain the most from the revamp and repair of roads, bridges, buildings, as well as the overhaul of cargo hauling and energy transformation on an almost unfathomable scale.

Uncover insights on How To Profit From Trillions on Spending for Infrastructure.

Keen to stay well-versed with the latest market moves? Embrace enlightenment with Zacks Investment Research’s 7 Best Stocks for the Next 30 Days.

For a more in-depth analysis of Cracker Barrel Old Country Store, Inc. (CBRL) – Free Stock Analysis Report, take a closer look.

Reflecting on the trials ahead, with an eye on potential rewards, venture forth into the stock market wilderness with conviction.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.