“`html

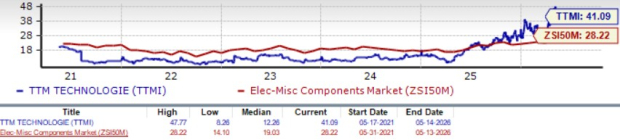

TTM Technologies (TTMI) shares are currently trading at a forward 12-month Price/Earnings (P/E) ratio of 41.09, significantly higher than the Zacks Electronics – Miscellaneous Components industry average of 28.22 and the Computer and Technology sector’s 25.87. The stock has surged 149.1% year-to-date, outpacing the Zacks sub-industry decline of 7.6% and the broader sector’s 17.3% increase. Key competitors like Sanmina Corporation and TE Connectivity have reported gains of 61.3% and declines of 9.1%, respectively.

TTMI’s revenue is heavily driven by AI data center infrastructure and defense modernization, which collectively account for 80% of its revenue. The company recorded a commercial book-to-bill ratio of 1.65 in Q1 2026, with its backlog expanding 52% year-over-year to $787 million. Revenue forecasts for 2026 sit at $3.83 billion, representing a 31.65% increase year-over-year, while the consensus estimate for earnings per share (EPS) is pegged at $3.60, suggesting a year-over-year growth of 46.34%.

However, TTM Technologies is facing concerns over cash flow, reporting a negative free cash flow of $85 million in Q1 2026 due to elevated capital expenditures. The company aims to expand its capacity with an increased 2026 capital expenditure guidance of $300 to $320 million, which could exert further pressure on cash generation in the short term.

“`

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.