Prologis Charts a Steady Course Amid Market Challenges

Prologis (PLD) stands to gain from its extensive network of modern logistics facilities positioned in key distribution hubs worldwide. The company’s significant scale and strategic acquisitions paint a promising picture for future growth. With a solid balance sheet, Prologis is well-equipped to pursue these opportunities.

Despite favorable industry conditions, Prologis has initiated a data center strategy that includes both warehouse conversions and new developments. In December, the company sold a data center project in Chicago to HMC Capital. Additionally, Prologis is collaborating with Skybox Datacenters to transform its Illinois warehouse into a high-capacity data center with a 32-megawatt capacity.

Nonetheless, challenges in the industrial real estate market and lower demand present hurdles for Prologis. Increased interest expenses contribute to the overall pressure the company is experiencing.

On January 21, Prologis will announce its fourth-quarter and full-year 2024 results. The real estate investment trust (REIT) has provided guidance indicating that its core funds from operations (FFO) per share for 2024 will fall between $5.42 and $5.46.

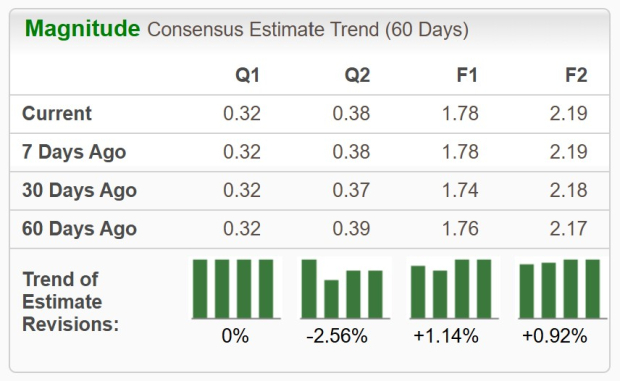

Analysts maintain a positive outlook on this Zacks Rank #3 (Hold) stock. Over the past two months, the Zacks Consensus Estimate for its 2024 FFO per share has been adjusted slightly upward to $5.45. For the upcoming fourth quarter, the consensus estimate stands at $1.38 per share.

Prologis shares have fallen by 3.2% over the last month, which is better than the industry average decline of 7.7%.

Image Source: Zacks Investment Research

What’s Driving Prologis Stock?

Prologis operates logistics real estate in some of the globe’s busiest distribution centers. The strong demand for its strategically situated facilities is crucial for its healthy operating performance. Even with a slowdown in the industrial real estate market, Prologis reported an average occupancy level of 95.9% in its portfolio during the third quarter. Management projects the average occupancy for 2024 will be between 96% and 96.5%. Our estimate for the fourth-quarter occupancy is 96.4%.

The company continues to expand in high-growth markets through targeted acquisitions and development projects. Over the years, Prologis has participated in major M&A transactions and engaged in smaller off-market deals. For 2024, Prologis predicts acquisitions in the range of $1.75 to $2.25 billion, along with development starts also projected at $1.75 to $2.25 billion.

Additionally, Prologis is tapping into the growing data center market by converting warehouses and developing new ones. They plan to open around 20 new data center projects over the next four years, with total investments estimated between $7 billion and $8 billion.

Prologis maintains a strong balance sheet with significant liquidity—$6.6 billion as of September 30, 2024. The company’s weighted average interest rate on its total debt stands at 3.1%, with an average maturity of 9.2 years. This financial strength positions Prologis well for future growth opportunities.

Consistent dividend payments attract REIT investors, and Prologis has shown its commitment in this area. In the last five years, the company has increased its dividend five times, leading to a five-year annualized growth rate of 13.66%. Given the company’s robust operating foundation and optimistic growth outlook, this dividend rate appears sustainable in the short term. Explore Prologis’ dividend history here.

What’s Challenging Prologis Stock?

In a volatile environment marked by high interest rates and geopolitical issues, clients are focused on cost management, which may delay their leasing decisions. Consequently, demand is expected to remain weak in the near term.

Though the Federal Reserve recently announced rate cuts, interest rates remain high—posing a continued concern for Prologis. Elevated rates lead to increased borrowing costs for the company, which can hinder its ability to acquire or develop properties.

As of September 30, 2024, Prologis’ consolidated debt reached $32.3 billion. Estimates for 2024 suggest a year-over-year increase of 32.5% in the company’s interest expenses.

Stocks to Watch

Other promising stocks in the broader REIT sector include Cousins Properties (CUZ) and SL Green Realty (SLG), both currently rated Zacks Rank #2 (Buy). You can view the complete list of Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Cousins Properties’ 2024 FFO per share has been slightly increased to $2.68 over the past two months.

Similarly, the Zacks Consensus Estimate for SL Green’s 2024 FFO per share has gone up to $7.83 in the last month.

Note: All earnings mentioned in this article refer to FFO, a critical metric for assessing REIT performance.

Free: 5 Stocks to Consider as Infrastructure Spending Increases

Trillions of dollars in federal funds are designated for upgrading and repairing America’s infrastructure. This funding will enhance not only roads and bridges but also AI data centers, renewable energy, and more.

Find out about five surprising stocks ready to benefit from the upcoming spending spree.

Download the guide on profiting from the trillion-dollar infrastructure boom for free today.

Prologis, Inc. (PLD): Access Free Stock Analysis Report

Cousins Properties Incorporated (CUZ): Access Free Stock Analysis Report

SL Green Realty Corporation (SLG): Access Free Stock Analysis Report

For the full article on Zacks.com, click here.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.