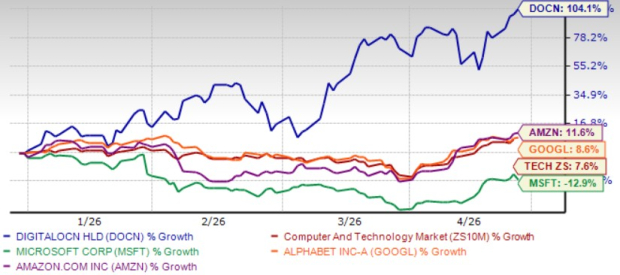

DigitalOcean (DOCN) has experienced a 104.1% return year-to-date, significantly outpacing the broader Zacks Computer and Technology sector, which returned 7.6%. As a developer-focused cloud provider, DigitalOcean plans to implement 31 megawatts of new capacity by 2026 to support at least 25% year-over-year growth. However, the company faces execution risks tied to supply chain management and capacity utilization.

Key financial data includes a projected remaining performance obligation of $134 million for Q4 2025, with $73 million expected to be recognized in the next year. The Zacks Consensus Estimate forecasts earnings at 27 cents for Q1 2026, reflecting a 51.79% year-over-year decline. DigitalOcean’s adjusted EBITDA margin is anticipated to be between 36% and 38% for 2026, although depreciation and lease expenses could pressure margins in the near term.

Despite a favorable demand environment for AI inference, DigitalOcean’s balance sheet is strained, with net leverage above 4X expected in the short term. Additionally, the company plans to buy back $312 million in 2026 convertible notes. Investors are advised to monitor utilization and profitability closely given the current high valuation and execution dependencies.