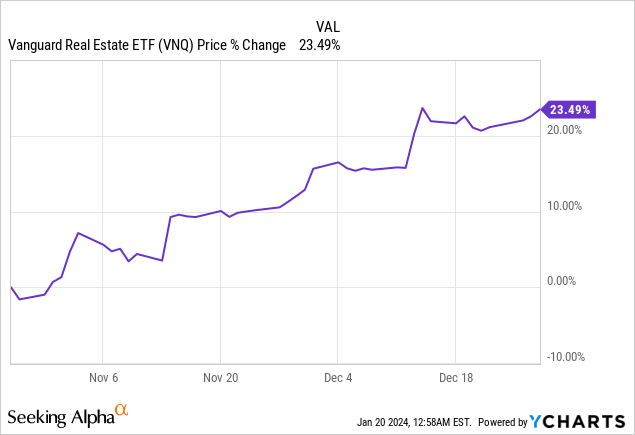

REITs (VNQ) soared in late 2023 upon the Fed’s announcement of at least 3 interest rate cuts in 2024.

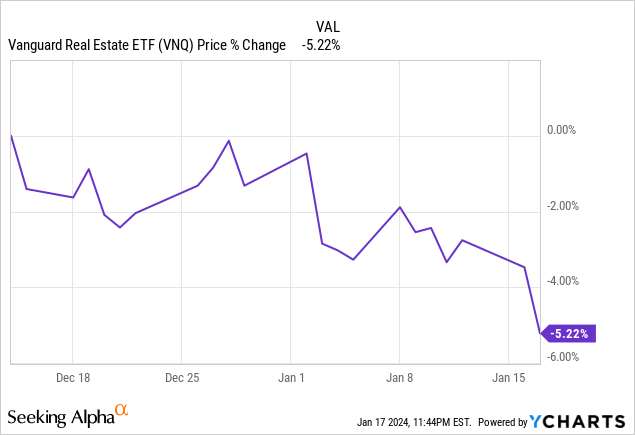

However, since then, REITs have experienced a significant dip, with some plunging to lower levels:

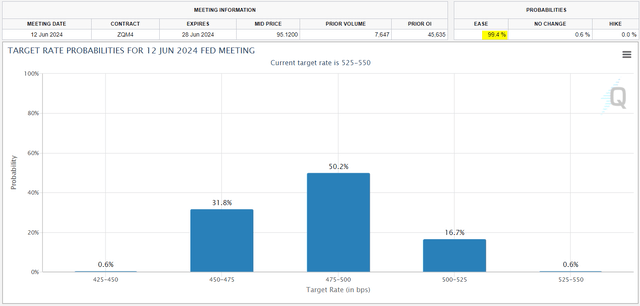

This presents a compelling opportunity as the expectations for lower interest rates remain unchanged, with a 99.6% chance of at least one rate cut by June according to the FedWatch tool:

The dip in REITs is not a reflection of a change in outlook, but rather shortsighted profit-taking by investors, oblivious to the fact that REITs remain heavily discounted even after the recent rally.

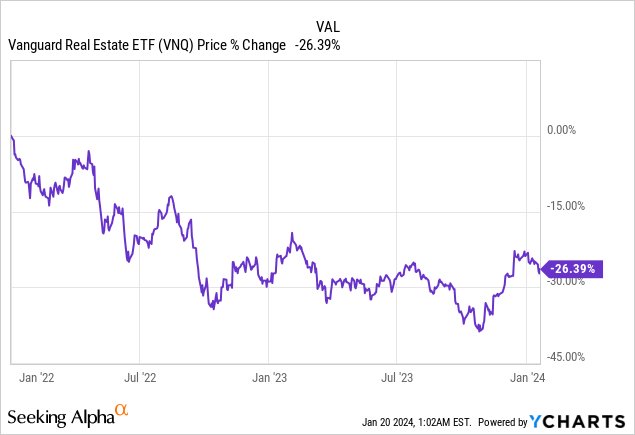

Currently down 26% over the past two years, despite a 5-10% increase in cash flows, many individual REITs have experienced even steeper declines:

The extensive decline is linked to investors finding solace in money market funds, yielding over 5%. Nevertheless, as interest rates are slashed, a significant influx of capital into REITs and other high-yielding equities is anticipated.

In light of this, it is prime time to amass more REITs, especially following the recent dip. Below are two “Buy The Dip” prospects:

Farmland Partners (FPI)

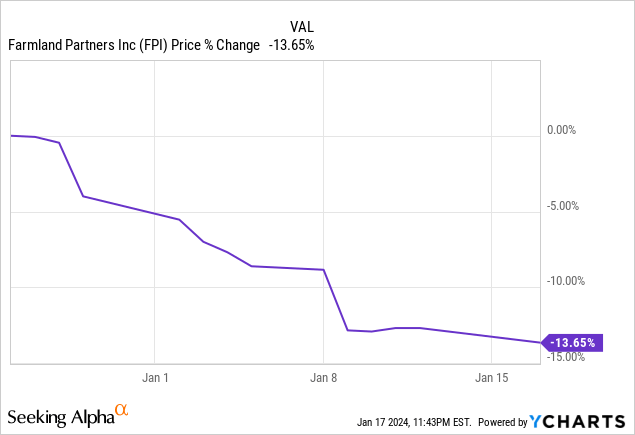

After a brief recovery to $13 per share, Farmland Partners has regressed to the low $11 range:

Priced at approximately $11 per share, FPI represents a compelling buy, with its net asset value estimated to hover around $18.

This signifies a ~40% discount to its net asset value. The unexpected drop in price is attributable to its descent alongside the REIT sector, despite farmland’s escalating worth.

Interestingly, the management is capitalizing on this disparity between public and private markets by selectively vendoring properties at premiums to their book value, and repurchasing shares at substantial discounts to their fair value.

In the past year alone, they revealed sales worth $120 million with an average 15% gain, utilizing the proceeds to buy back shares and pay off debt—remarkable for a company with a $550 million market cap.

Additionally, the chairman and former CEO of the REIT invested another million in stock with personal funds, despite already being heavily invested:

Their optimism stems from the opportunity to acquire farmland equity at 60 cents on the dollar.

Farmland has consistently been a superior investment over time, garnering even higher returns than the S&P 500 (SPY). Procured at a considerable discount, it becomes an even more lucrative investment.

As interest rates revert to lower levels, a resurgence of confidence in REITs should be particularly beneficial to lower-yielding REITs like FPI, potentially yielding a 30-50% upswing in a future recovery. Should the share price not rebound, the company will persist selling assets to repurchase shares, and ultimately might decide to sell the entire company to unlock its value

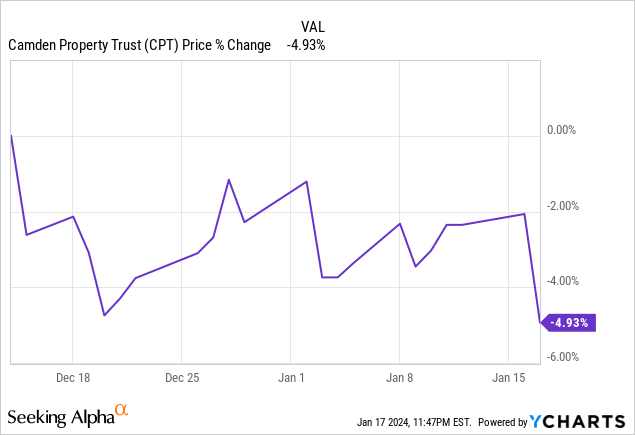

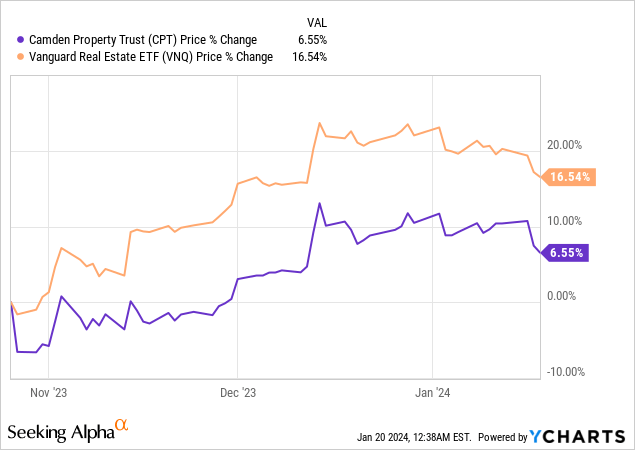

Camden Property Trust (CPT)

Camden realizes the plight of REITs as it finds itself in a similar predicament to Farmland Partners, with a potential upside as its share price converges with its net asset value. An opportune moment has presented itself to investors as these REITs offer compelling bargains.

Cautious Optimism For Apartment REITs Amid Market Volatility

Property Trust is a familiar name in the realm of apartment Real Estate Investment Trusts (REITs). Amid the volatility in the market, it didn’t suffer as much as Farmland Partners. However, its initial rise wasn’t as meteoric. Presently, it’s down by 5%, a figure that resonates with the overall REIT market. Despite this, the company has shown resilience and an ability to hold its ground amidst market turbulence.

Amidst this recent underperformance, one of the factors contributing to this trend is the surge in loan delinquencies within the apartment sector. Many private equity landlords find themselves overleveraged as a result of increasing interest rates. Operating with 60-70% variable debt, these landlords are under immense pressure, especially considering the deceleration in rent growth. The apartment sector is facing challenging times and navigating uncharted waters.

As the storm rages, well-capitalized apartment REITs like Camden Property Trust are emerging as beacons of resilience. With its Loan-to-Value (LTV) ratio hovering around 30% and an enviable balance sheet, it is primed to capitalize on distressed property sales at deflated prices. Mid-America (MAA), another prominent apartment REIT, has already capitalised on an enticing deal in Q3, securing property at an advantageous price point.

Contrary to popular belief, the recent surge in loan delinquencies presents a net positive for REITs such as Camden Property Trust. While it may cause a slight dent in property values in the short term, the company’s A-rated balance sheet positions it to snatch up distressed assets at discounted rates, ultimately benefiting shareholders over the long haul.

The market has attributed a ~35% markdown to Camden’s net asset value, a remarkable discount for a blue-chip apartment REIT boasting a fortress balance sheet and a lengthy track record of substantial outperformance.

Expectantly, the weakness prevailing in the apartment sector is likely to persist for another year or two. However, every cloud has a silver lining. The stalling of new development projects has paved the way for a potential resurgence in growth, with expectations set for a revival in 2025-2026.

As the narrative of growth unfolds, and interest rates regress to lower levels, Camden is projected to recalibrate towards its net asset value, unlocking a potential upside of 30-50%. In the interim, investors can relish a 4% dividend yield, and the company will continue its strategic acquisition of new assets to bolster value and augment its cash flow.

Closing Thoughts

If you missed the boat on REIT buying opportunities in 2023, rest assured, a second chance is presenting itself with discounted REITs following their recent slump. However, this window of opportunity is slowly but surely closing. As interest rates are anticipated to regress to lower levels, the resurgence of REITs is on the horizon, potentially propelling them to much loftier heights.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.